At AlbaCore, we focus on the long-term. As one of Europe’s leading alternative credit specialists, we invest in private capital solutions, opportunistic and dislocated credit, and structured products.

Discover moreInvestment strategies

Insights

Our philosophy is very simple. We are constantly searching for high quality businesses and when we acquire them, we will work relentlessly with them to create long-term sustainable value through innovation, ESG-led and proactive asset management.

Discover moreInvestment strategies

Insights

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

Specialists in equity portfolios in Asia Pacific, emerging markets, global and sustainable investment strategies

Discover more

Introduction

- Global listed infrastructure underperformed in 2023 owing to rising interest rates and a shift away from defensive assets. Relative valuations are now at compelling levels.

- Infrastructure assets are expected to see earnings growth in 2024 and beyond, aided by structural growth drivers, especially utilities which are benefiting from energy transition.

- Infrastructure capital expenditure should accelerate in 2024, despite a higher cost of capital.

- Political and regulatory risks remain elevated but reduced customer bill pressures should provide some relief

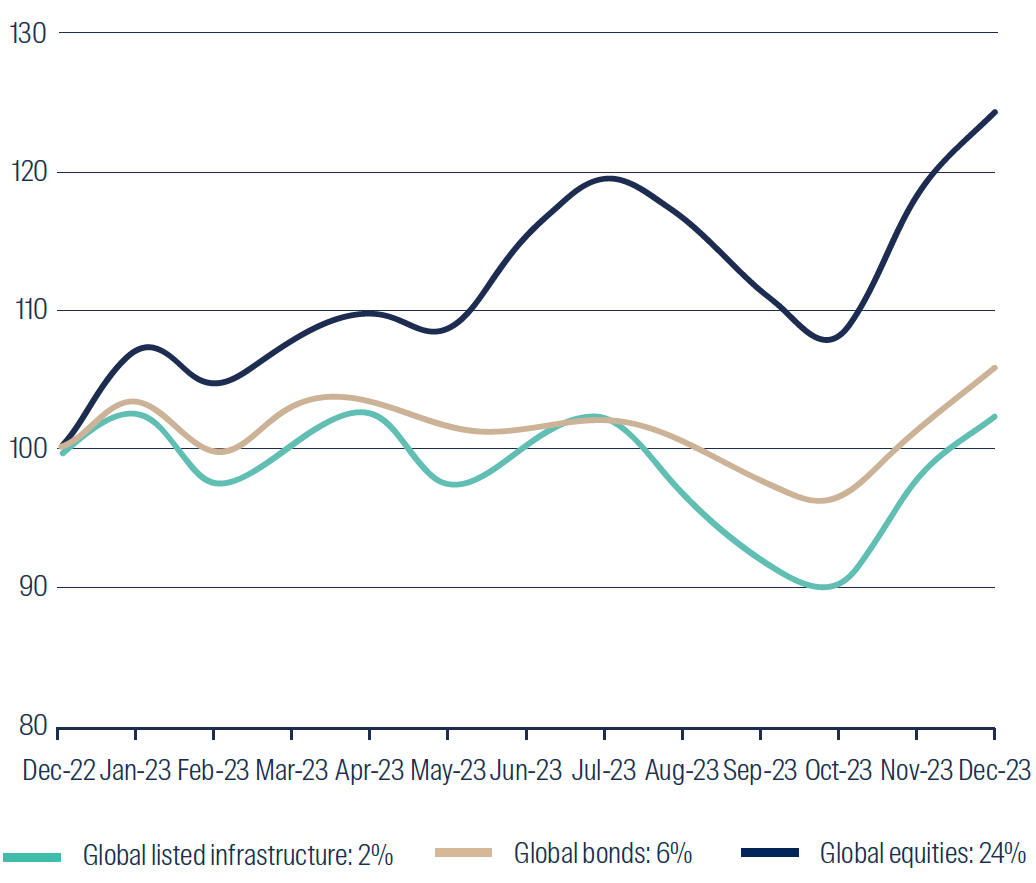

Global listed infrastructure (+2%) underperformed both global equities (+24%) and global bonds (+6%) in 20231. Despite increased earnings and solid fundamentals, a sharp rise in real bond yields saw infrastructure valuations fall materially during the year. This paper provides analysis of the key drivers of performance in 2023 and offers an outlook for the year ahead. Additionally, while all investing carries risk, it explains why we believe that now is an opportune moment to consider investing in global listed infrastructure, highlighting the compelling reasons for doing so.

Global infrastructure, equities and bonds performance CY 2023

Global Listed Infrastructure: FTSE Global Core Infrastructure Index 50/50 Net TR (USD)

Global equities: MSCI World Net TR Index (USD)

Global Bonds: Bloomberg Global Aggregate TR Index Value Unhedged (USD)

Source: First Sentier Investors. Data to 31 December 2023

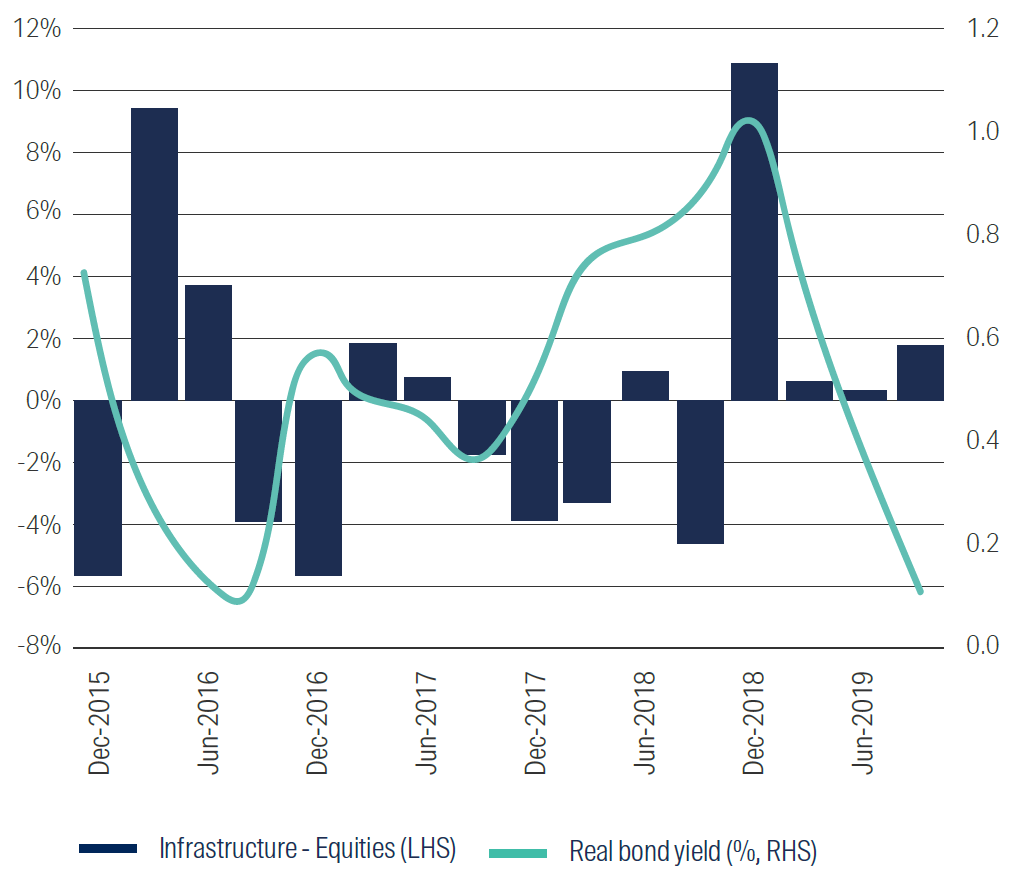

The recent period of global listed infrastructure underperformance is not unprecedented. In 2018, for example, infrastructure returns were adversely affected by a rise in real bond yields, but the asset class then bounced back as rates started to decline. With the likelihood of rates having now peaked in many markets, global listed infrastructure has the potential to outperform in the year ahead.

The relationship between real bond yields and the relative performance of global listed infrastructure and global equities, between 2016 and 2019, is illustrated in the following chart.

Infrastructure outperforms as real yields fall

Source: Bloomberg, First Sentier Investors

Chart covers the period between December 2015 and September 2019.

Year in review

Having held up well in 2022, global listed infrastructure underperformed global equities during 2023. This appeared to be primarily a reflection of macro factors. Rising interest rates weighed on infrastructure valuations as central banks adopted a “higher-for-longer” narrative. This triggered a sharp rise in government bond yields, with the US 10-year real bond yield reaching multi-year highs. Meanwhile, inflation, which listed infrastructure assets can usually pass on to the end user, subsided. The asset class was also affected by a widespread shift towards higher beta sectors such as technology and themes such as artificial intelligence.

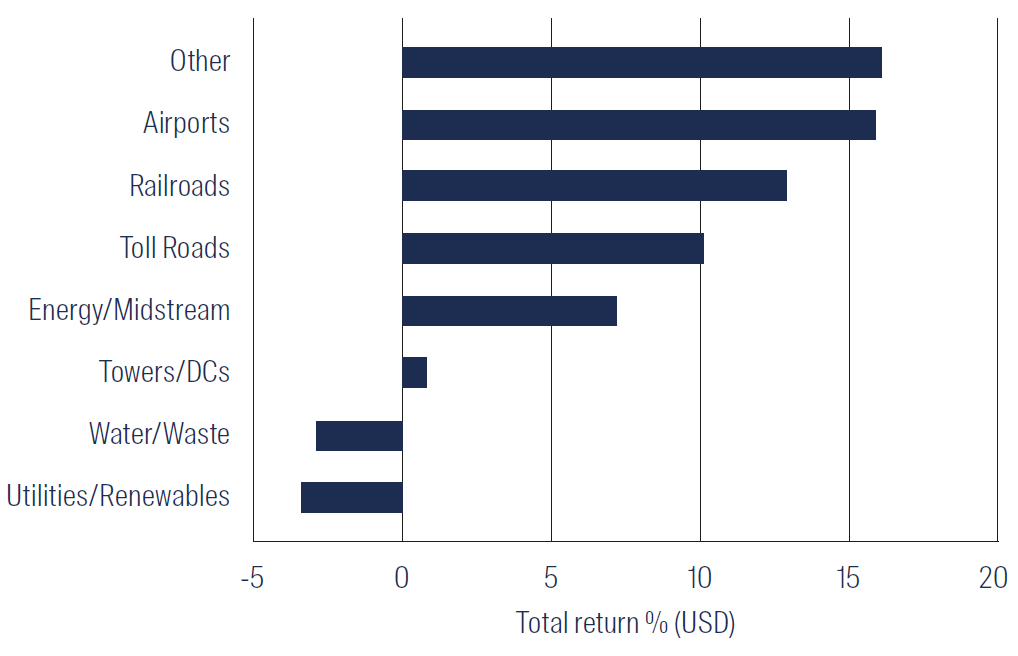

Transportation infrastructure such as Airports, Railroads and Toll Roads performed well in 2023. Airports in Europe and Latin America experienced gains as passenger volumes approached, and in some cases, exceeded pre-pandemic levels. Toll roads were supported by robust traffic volumes and the appeal of inflation-linked tolls. Passenger rail companies in Japan enjoyed the benefits of a return to office and strong leisure travel on their networks.

Elevated geopolitical tension underscored the importance of energy independence and security. Against this backdrop, the Energy Midstream2 sector delivered another year of solid performance, bolstered by elevated commodity prices and strong demand for US Liquefied Natural Gas (LNG) exports. As a reliable and relatively cheap producer, additional long-term contracts for US LNG are likely in the coming years.

On the negative side utilities lagged, with renewables-focused utilities underperforming on concerns that higher borrowing costs may make it harder to fund renewables projects. Mobile Towers came under pressure in 2023, owing to concerns that telecom companies (towers’ main customers) may slow investment in their networks. Tower companies typically have fixed escalators built into their contracts, but less ability to pass through higher interest costs.

Global infrastructure performance by sector | CY2023 |

Source: Bloomberg and First Sentier Investors

Based on FGCI index weights. Data as at 31 December 2023

Infrastructure’s inflation pass-through is working well, supporting earnings across the asset class. It can take time for this inflation pass-through to take effect. Toll road companies typically increase their prices every quarter, but US utilities need to wait until they re-negotiate with the regulator to pass through costs, which can take one to two years. This proved challenging for some companies, given the rapid rise in real bond yields in 2023.

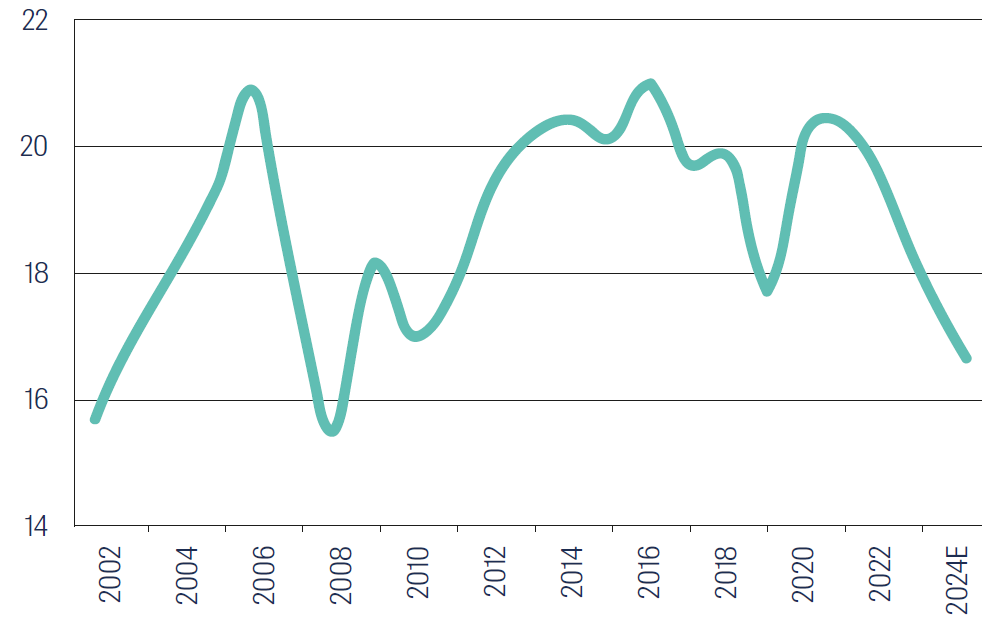

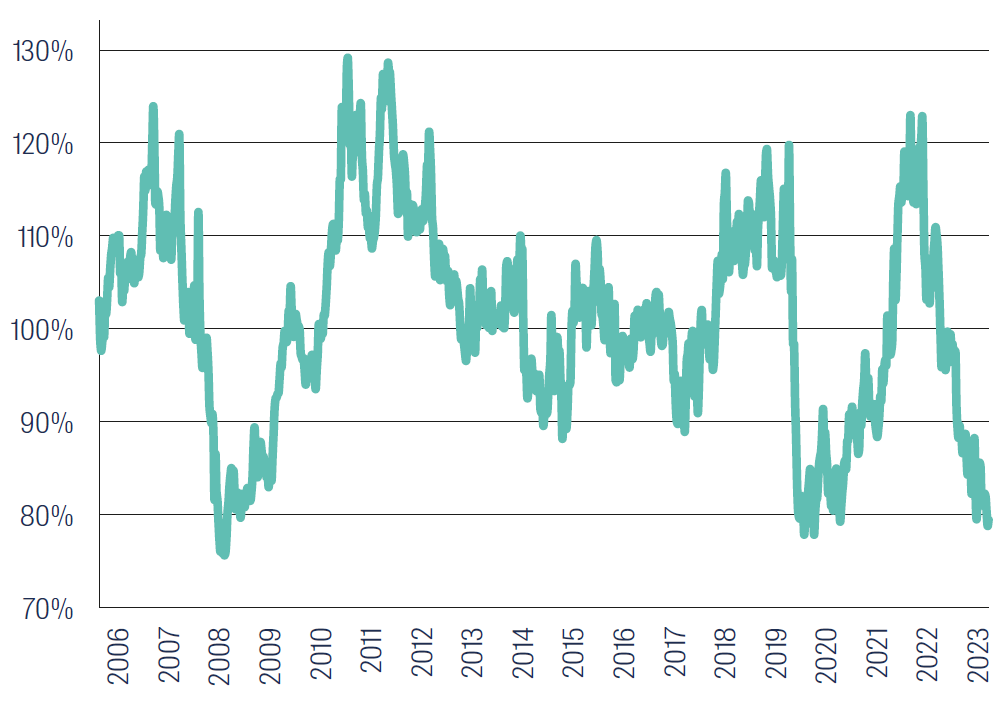

We believe valuations are now compelling, with many global listed infrastructure companies trading at levels not seen since the global financial crisis.

Global infrastructure | Price/Earnings x |

Source: Bloomberg and First Sentier Investors

Simple avg of 250 stocks in universe. Data as at 31 December 2023

Outlook

The early part of 2024 may present challenges for broader markets, including slower economic growth, operating expenditure inflation and higher interest costs. We believe a recession is still a possibility, with markets overly optimistic and recent global equity returns largely driven by the “Magnificent Seven3” tech stocks. Overdependence on such a narrow set of stocks can be risky, leaving markets vulnerable to a downturn if their fortunes were to falter. In our view, infrastructure provides a significant and cheap diversifier within a portfolio.

Despite these potential headwinds, we continue to see positive earnings revisions for infrastructure companies. For example, utilities have the ability to pass through inflation, while the transition to lower carbon sources of energy generation is presenting them with opportunities for rate base and earnings growth. Overall, we anticipate upside earnings risk for listed infrastructure.

The following chart illustrates how US utility earnings have held up since early 2022, compared to the broader US market.

Earnings resilience | 2022/23 |

Source: Bloomberg

Data as at 31 December 2023.

Infrastructure capital expenditure growth is likely to gain momentum in 2024, even in the face of a higher cost of capital environment. We anticipate that corporations will increase equity raisings while reducing buybacks to fund this acceleration in capital expenditure. This strategic shift should lead to greater investment in growth opportunities.

Political and regulatory risk are likely to remain elevated, given the US presidential election year and elections expected in more than 40 countries, including the UK, India and Mexico. For utility stocks, reduced customer bill pressures should provide some relief to this political risk. One area that we remain watchful of is the 2022 Inflation Reduction Act (IRA). The IRA is a United States federal measure passed by the Democrats which provides long-term tax incentives for clean energy projects, and which is expected to be supportive of regulated US utilities’ earnings growth over the years ahead.

The IRA is not subject to annual renewal (which previous clean energy subsidies were), or to voting to increase the US debt ceiling. However if the Republican Party (the GOP) were to win majorities in the US House of Representatives and the US Senate, as well as the Presidency, it would be in a position to reverse this legislation.

Even if it were able to, the GOP’s appetite to do so is likely to be low. The majority of the US’ renewable energy projects, which are set to benefit from the IRA, are located in GOP states (for example Texas, Oklahoma, Arizona, Kansas, Missouri, Iowa etc.). There could be some risk to funding for projects with more marginal economics e.g. offshore wind and hydrogen, but overall the risk to the IRA appears to be small.

Mergers and acquisitions (M&A) activity levels could accelerate in 2024 as private market funds buy discounted listed infrastructure assets, and as listed infrastructure companies sell non-core assets to fund higher growth capital investment needs. This could lead to consolidation and increased competitiveness within industries.

In our opinion, balance sheets remain under-geared in Asia, while those in North America and Europe are fairly geared. We expect leverage to remain a focus in 2024, with the market penalising companies that need to borrow or raise equity to fund growth. It is worth noting that debt maturity remains strong at over 12 years on average for the holdings in our global strategy today4.

We take a closer look at the sector outlook for the asset class in the section below.

Utilities (~50% of our global strategy)

After a difficult 2023, utilities and renewables stocks face a more constructive outlook in 2024. We believe earnings risks are poised slightly to the upside. Capital expenditure growth should accelerate, reflecting the need for increased resiliency spend and higher electricity usage growth from data centres, industrial on-shoring and electric vehicles. Customer bill pressures are declining, balance sheets are in better shape going into 2024 and we could see a re-emergence of M&A activity. However we also expect to see increased equity issuance to help fund higher capital expenditure.

Renewable energy investment is expected to rebound after a trifecta of bad news in 2023, including cost increases stemming from China sanctions and COVID-19, Inflation Reduction Act (IRA) delays and a sharp increase in the cost of capital. These factors, combined with a potentially favourable interest rate environment and the sector trading at a large discount to its historic relative trading earnings multiple, set the scene for a constructive year.

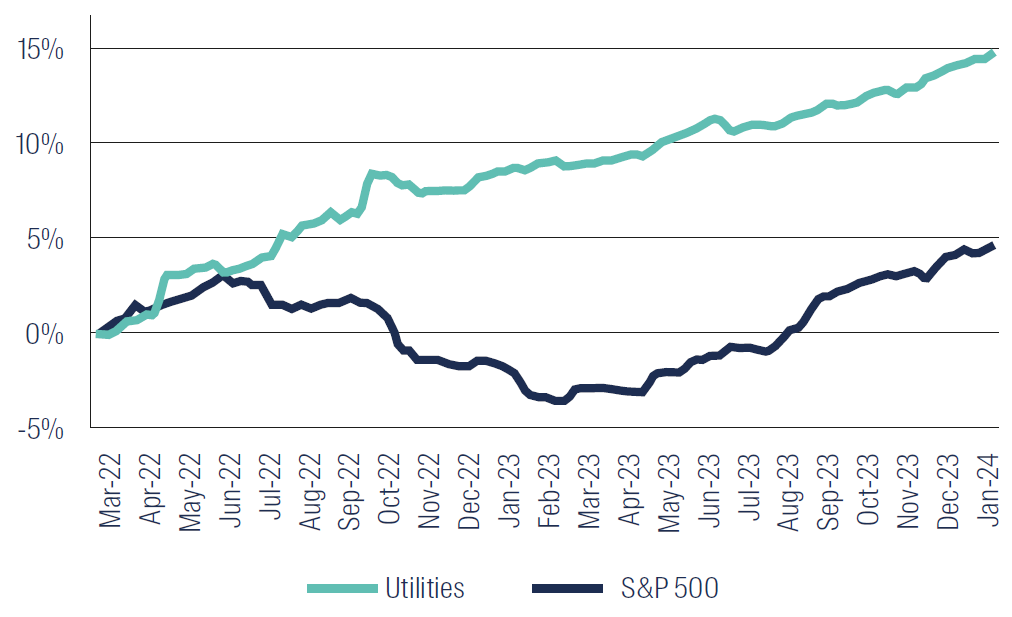

US utilities valuations relative to S&P 500

Source: Bloomberg, First Sentier Investors

Data as at 31 December 2023.

Overall, the IRA has increased the earnings growth potential and visibility of US utilities, which represent around 40% of our global strategy. Integrated and regulated utilities operating in US states with strong renewable resources (solar in the south, wind in the mid-west) and good or improving regulation should be key beneficiaries.

Transportation (~30% global strategy)

Toll roads have benefited from the modal shift from passenger rail to cars since COVID-19, with inflation escalators in tolling having little impact on demand from road users. Strong operating leverage further supported positive earnings growth during the year. Improvements to road networks during the COVID-19 period lead us to believe that there will be strong traffic growth beyond 2019 levels, as congestion returns to major cities and road users make use of these enhanced assets. We maintain an overweight position in the sector and remain positive looking ahead into 2024.

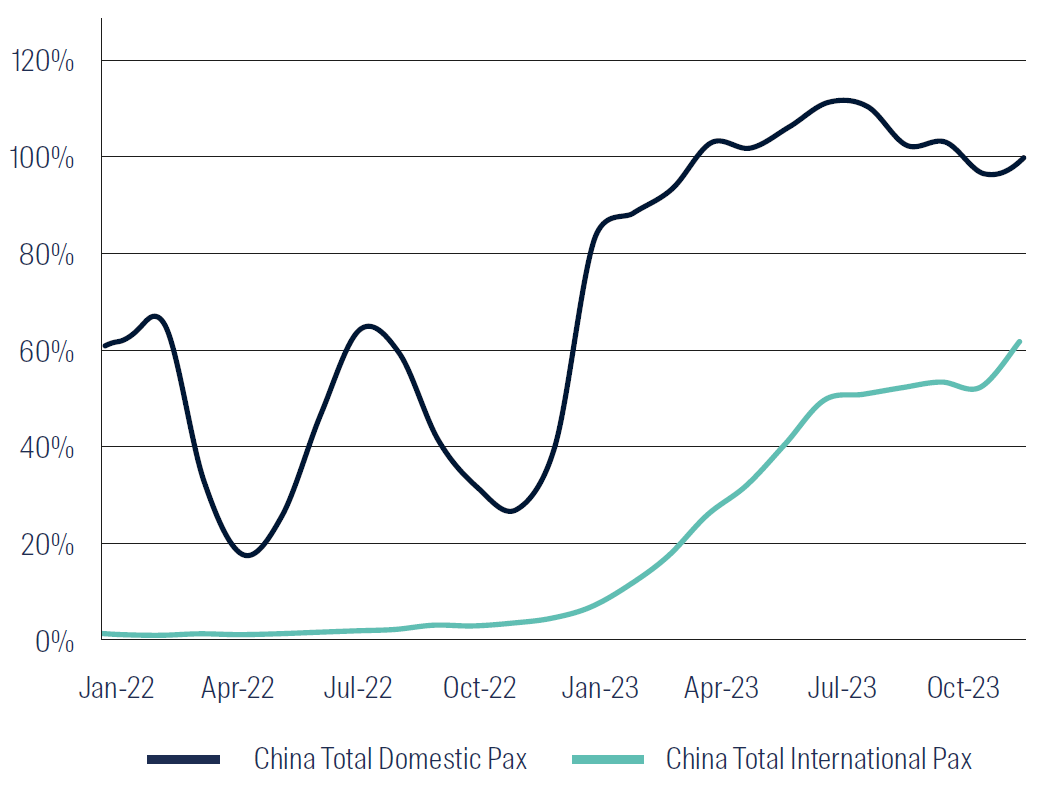

In 2023, airports experienced a significant increase in passenger traffic as the COVID-19 recovery gathered pace, approaching pre-pandemic levels. Leisure-orientated airports outperformed, owing to pent-up travel demand5. In 2024, we anticipate a recovery in retail spending by Chinese travellers and a gradual improvement in business traffic. However, cost-of-living pressures may constrain leisure travel, resulting in slower growth than in 2023. Therefore, we remain selective within the sector, but have identified what we believe to be attractive mispricing opportunities for 2024.

COVID Recovery by Traveller Type (vs 2019 comp.)

Source: Company Reports, First Sentier Investors

The freight railroad sector saw an improvement in performance in 2023 as volumes turned positive towards the end of the year. We anticipate this trend to continue into 2024, driven by improved service and a reduction in inventory destocking. Despite the challenges faced, the sector's pricing power remains strong, and as costs stabilize, we expect to see margin improvement in the second half of 2024. This combination of volume growth and margin improvement has the potential to lead to a positive re-rating of valuations for North American railroads in 2024.

Communications (~10% global strategy)

The mobile tower sector faced challenges in 2023 owing to higher interest rates and slower domestic leasing activity. Their main customers (telecom operators) continued to roll out 5G but at a slower pace than previously expected. With leverage for tower companies higher than other sectors, balance sheets have been a focus. Over the year ahead, we expect the 5G rollout to continue, leading to incremental demand for tower leasing and improved valuations.

Data centre leasing activity remains mixed, with early signs of Artificial Intelligence (AI)-related demand offset by customer footprint optimization. Although there have been modest additions to supply, robust demand has swung pricing in favour of the data centre operators.

Energy Midstream (~10% global strategy)

Buoyant energy prices, increased natural gas exports and disciplined capital expenditure saw the North American energy midstream sector produce strong free cash flow (FCF) in 2023, further enhancing already-robust balance sheets. In the absence of substantial new investment opportunities, we expect the sector to use its FCF for increased dividends, buybacks and selective M&A in 2024.

The energy crisis that followed Russia’s 2022 invasion of Ukraine reminded the world that only when energy is affordable and secure can it be truly sustainable. Natural gas is expected to play a crucial role as a transition fuel in various parts of the world, especially in developing countries. Within the US, extreme weather events, the closure of coal fired power plants and delays in the buildout of new renewable generation means natural gas has increasingly been called upon to provide stability and reliability to the electric grid. This domestic demand, combined with rising LNG export levels, is underpinning the financial health of the energy midstream sector.

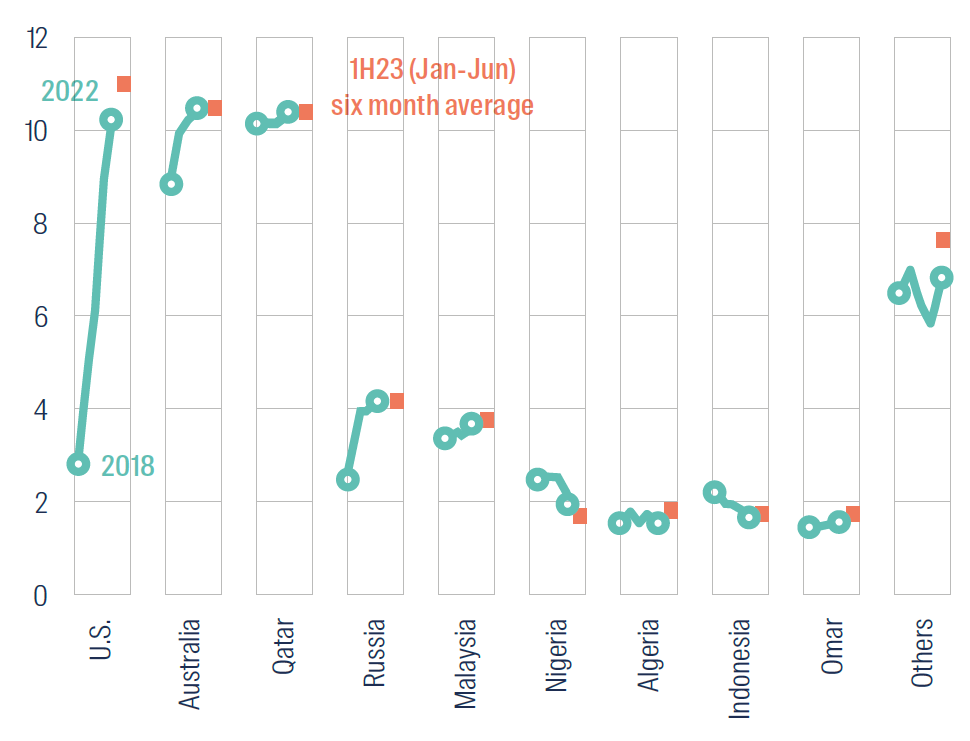

Global liquefied natural gas exports by exporting country (Jan 2018-Jun 2023)

Billion cubic feet per day

Source: EIA. Data as at 30 June 2023

Why now?

The following six reasons outline why we believe listed infrastructure is well positioned to outperform in the year ahead:

- Interest rates – may have now peaked, as many central banks have paused their tightening cycles. Rising interest rates have been an asset class headwind which could turn into a tailwind very quickly.

- Valuations – listed infrastructure has delivered broadly flat returns over the past two years, despite resilient earnings growth. We believe valuations are now at appealing levels.

- Macro risks – despite rising bond yields, slowing consumer spending and wars in Europe and the Middle East, broader equity markets traded close to all-time highs in 2023. Listed infrastructure, which is less sensitive to the global economy, could now serve as a defensive diversification tool.

- Renewables outlook – supply chains are easing and construction costs decreasing. In the US, IRA benefits have taken time to execute but are expected to support earnings upgrades for US utilities over the medium term.

- Private markets – demand for infrastructure assets in private/ unlisted markets remains strong, and valuations are well above listed markets. This provides an element of downside protection for investors.

- Earnings growth – we expect the asset class to deliver EBITDA, EPS and DPS6 growth of between 6% and 7% per annum over the next two years, despite a potentially challenging economic backdrop.

Conclusion

In 2023, global listed infrastructure underperformed global equities due to rising interest rates and a shift away from defensive assets. However, earnings growth for critical infrastructure assets is expected to be underpinned by structural growth drivers in 2024 and beyond, particularly for utilities that are deriving earnings growth by investing in the energy transition.

Infrastructure’s inflation pass-through is working well and supporting earnings across the asset class. Valuations are now appealing, and earnings have proved resilient.

We believe the mix of inflation-linked income (a yield of between 3% and 4%) and structural growth (expected earnings growth of between 6% and 7%) offered by the asset class will prove attractive to investors in the years ahead.

The First Sentier Global Listed Infrastructure team remains focused on bottom-up stock picking, seeking mispriced, good quality companies trading at attractive relative valuations.

Global Listed Infrastructure

Infrastructure powers the world we live in – and when it comes to on-the-ground research, our team can be found on site

Investing in global listed infrastructure can offer inflation-protected income and steady capital growth from real assets delivering essential services. We search for best-in-class assets worldwide with high barriers to entry, structural growth and pricing power.

1 All data in USD terms. Performance numbers reference the FTSE Global Core Infrastructure 50/50 Index, Net TR, the MSCI World Index, Net TR and the Bloomberg Global Aggregate TR Index, Value.

2 Oil & gas storage & transportation.

3 The seven largest US tech stocks: Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, Nvidia, Tesla.

4 As at 31 December 2023.

5 Source: First Sentier Investors; company data.

6 Earnings Before Interest, Taxes, Depreciation and Amortisation; Earnings Per Share; Dividends Per Share

Source: Company data has been retrieved from company annual reports or similar investor reports. Financial metrics and valuations are from Bloomberg. As at 31 December 2023 unless otherwise noted.

Read our latest insights

Important information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure.

Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward-looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Investors' portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Investors.

This document is not, and under no circumstances is to be construed as, an advertisement or a public offering of the fund in Canada. No securities commission or similar authority in Canada has reviewed or in any way passed upon this document or the merits of the fund described in this document, and any representation to the contrary is an offence.

Selling restrictions

Not all First Sentier Investors products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Investors in order to comply with local laws or regulatory requirements in such country.

This material is intended for ‘professional clients’ (as defined by the UK Financial Conduct Authority, or under MiFID II), ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) or Financial Markets Conduct Act 2013 (New Zealand) and ‘professional’ and ‘institutional’ investors as may be defined in the jurisdiction in which the material is received, including Hong Kong, Singapore, Japan, and the United States, and should not be relied upon by or be passed to other persons.

The First Sentier Investors funds referenced in these materials are not registered for sale in the United States and this document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Investors.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors, FSSA Investment Managers, Stewart Investors, Realindex Investments and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), Realindex Investments (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business divisions of First Sentier Investors (Singapore).

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167)..

- Other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

|  |

|---|