At AlbaCore, we focus on the long-term. As one of Europe’s leading alternative credit specialists, we invest in private capital solutions, opportunistic and dislocated credit, and structured products.

Discover moreInvestment strategies

Insights

Our philosophy is very simple. We are constantly searching for high quality businesses and when we acquire them, we will work relentlessly with them to create long-term sustainable value through innovation, ESG-led and proactive asset management.

Discover moreInvestment strategies

Insights

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

Specialists in equity portfolios in Asia Pacific, emerging markets, global and sustainable investment strategies

Discover more

- Substantial renewable capex opportunities meet substantial execution challenges

- UK water utility periodic regulatory reset presents opportunities and headwinds

- China economy re-opening weaker than expected

In September 2023, I met more than 30 global listed infrastructure companies and stakeholders from the UK, Europe and China. The following travel diary summarises my impressions and findings from these meetings.

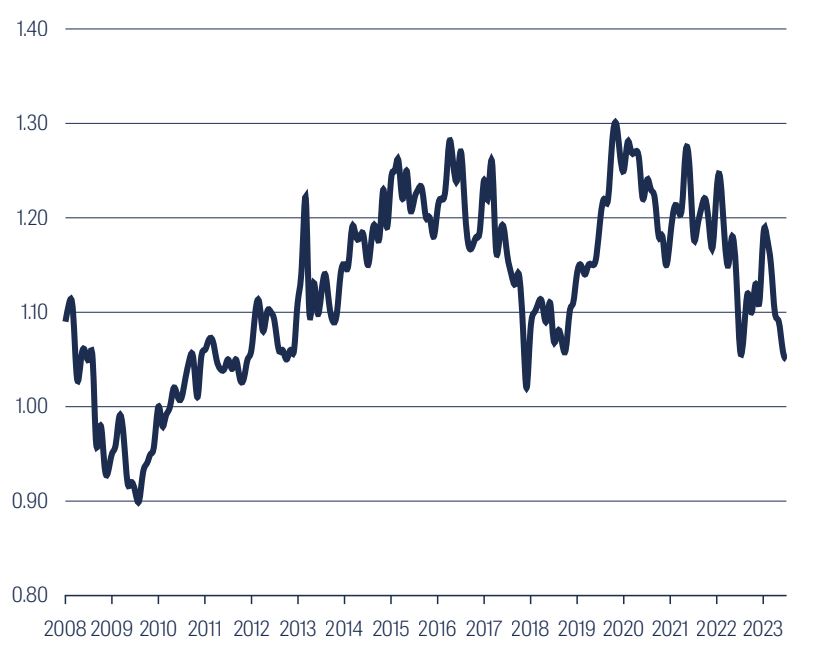

Europe & UK regulated gas, electricity transmission and distribution (T&D) and water utilities have relative greater ability to pass-through inflation within the GLI universe

Typically, this manifests itself via the annual adjustment of the regulated asset base (rate base) of the utility, which is often allowed to grow at a similar rate to that of the prevailing inflation rate. The trade-off for this benefit is usually lower allowed returns. As a result of this ‘real’ return + inflation adjustment framework, the long-term nominal returns for regulated utilities from these regions are generally comparable to those of similarly regulated assets from other parts of the world.

Over the past 18 to 24 months, this inflation link has provided a positive tailwind to the equity value of European and UK utilities, somewhat mitigating the headwind of rising nominal interest rates. With disinflation now appearing in Europe and the UK, we expect capex1 to take over from inflation again as the primary driver of rate base growth for these companies. We expect the push towards electrification to provide substantial investment opportunities for electric T&D utilities, as much of the world transitions to a lower-carbon society. For UK water companies, the capex focus, and hence investment opportunity, lies in the need to upgrade systems in order to improve environmental performance.

UK and EU inflation (% change, year over year)

| Source: Bloomberg, FSI as at 31 August 2023. | UK CPIH, EU CPI |

New renewable electricity resources…

We believe electric utilities are at the forefront of the transition from fossil fuel-based electricity generation to renewable generation sources. With supportive policy targets now in place, there is much work to be done to deploy new generation.

Participants include incumbent integrated utilities (companies that own regulated-return T&D networks as well as market-orientated generation and supply assets), pure-play renewable developer operators, financial investors and oil & gas majors.

We are still in the relatively early stages of renewables development. Accordingly, pure-play renewables developer/ operators that are big enough for institutional investors to invest in are few and far between. Further, as these developers are in the process of building assets to harvest cash flows over the next 20 to 25 years, there are meaningful demands on their balance sheets at this point in time. Significant renewables project pipelines present opportunity over time and should help to de-risk the equity story – if they are executed on time and on budget. However in the current environment of rising materials costs and supply chain pressures, the ability to do so is proving challenging, and was a hot topic during my research trip.

Renewables industry bellwether Ørsted recently wrote down a portion of their US offshore wind developments owing to rising costs and a nascent supply chain, amongst other things. In recent years, Ørsted has been awarded PPAs2 to supply electricity to local utilities for an agreed price per MWh3 (some with fixed escalators, some no escalators). However in the time it has taken to progress towards a final investment decision, the economics of these projects have been severely squeezed by higher capital costs, supply chain issues, rising interest rates and lack of transparency around tax incentives. In fact, conditions have deteriorated to such an extent that other players have simply opted to walk away from other projects for similar reasons.

For bottom-up fundamental investors such as ourselves, the takeaways here are:

- be discerning with each renewables project and understand how far advanced each one is in its development, contracting and construction life cycle, and

- be cautious about companies that are entering new markets and building supply chains from scratch.

...need to be connected to the grid too

While the build-out of wind and solar farms has attracted much attention (and this portfolio manager must admit that a solar farm is much more visually appealing than a set of transmission lines), it is worth remembering they need to be connected to the grid in order to deliver electricity to the end user. In fact, some industry participants have suggested that for every dollar spent on generation assets, up to a dollar may be required in T&D capex.

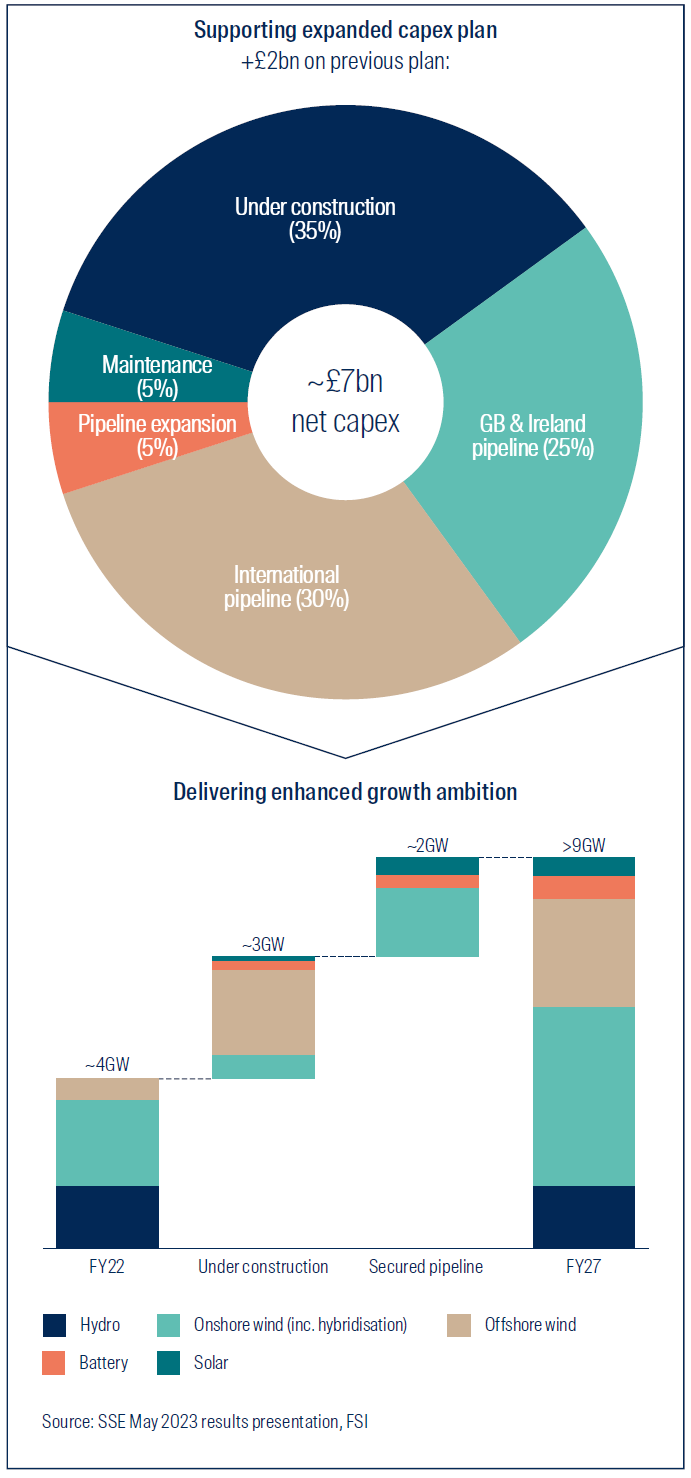

At this point in time, we prefer to gain exposure to this investment theme through incumbent integrated utilities which offer the prospect of capex growth both through network investment and through the building of new generation projects. UK-based SSE provides a good example of this. SSE is building on – and off-shore wind projects predominantly in the UK and Ireland, typically with 15-year CFD4 contracts. CFDs provide stability around the real price per MWh of electricity, meaning that the operator takes on the variability of the amount of electricity produced whilst being able to adjust by inflation. Several of SSE’s in-construction wind projects are now nearing completion. We came away with the impression that management was comfortable about their ability to deliver on these.

SSE Electricity Transmission RAV (£ bn) | Gross 100% basis |

| Source: Company reports, FSI as at 31 May 2023. RAV = Regulated Asset Value | G = SSE growth targets |

SSE also has a substantial and growing footprint of electricity T&D assets in the UK. These networks provide a base of relatively stable and predictable earnings, which can be balanced against the development and construction risks of new generation. Furthermore, the company’s network assets are remunerated in real terms (adjusted for inflation), further mitigating inflationary pressures.

Illustration of SSE’s renewable generation development plans

UK water utilities

Similar to their electric utility cousins, water utilities earn a real return with inflation adjusted for in the rate base. Water tariffs, operating expenditure and capex are set every five years under UK regulation using a process called a “price review”. Each price review provides an opportunity for the industry and its regulators (Ofwat is the key economic regulator for the UK water sector) to assess the areas of investment over the next period, whilst balancing up the appropriate cost of capital and customer bill profile. At the time of writing, we are approximately half-way through the sector’s current price review (PR24).

Equity markets dislike uncertainty. What will the new cost of capital be? Will the regulator allow the companies to add all the capex they ask for to their respective rate bases? Will they be stricter on borrowing and dividend payouts? As such, the Enterprise Value/rate base multiple that these stocks trade on have, in the past, usually de-rated as a price review has been carried out.

Severn Trent Enterprise Value/RCV

| Source: Ofwat, Bloomberg, FSI as at 30 September 2023. RCV: Regulatory Capital Value | One year Forward RCV |

Exogenous events also influence sentiment around the time of the price review. In the previous price review (PR19), the opposition Labour Party’s manifesto contained an ambition to nationalise the water utilities. In the current price review, Ofwat and UK Environment Agency reviews into operating standards/performance and the potential for financial penalties have weighed on sentiment. History doesn’t repeat but it rhymes.

It is clear, in our opinion, that the appetite exists for the water industry to greatly improve its operating performance; and that more capex will be required to enable this (for example, to separate previously combined stormwater and sewage pipeline networks). However, under the regulated model, additional capex will place upward pressure on customer bills. (Listed water companies are proposing a 22-37% real increase between 2025 and 2030, with inflation on top). It will be a challenge for Ofwat and the water companies to thread the needle of allowing a step-up in capex whilst maintaining politically-palatable water bill increases as they move through the price review.

Balance sheets have been a concern for the sector recently, especially if we consider the high-profile issues facing the largest water company, Thames Water and the equity raise from Severn Trent to coincide with their business plan. With projected gearing around 63% of rate base (for the three main listed UK water utilities – Severn Trent, United Utilities and Pennon), and the proposal from Ofwat to notionally use 55% for the next regulatory period, this further clouds the capex outlook.

We believe valuations in this space are starting to look interesting, but remain cautious about the potential headwinds facing the UK water sector, especially given it is likely that the draft determination of the PR24 price review may overlap with a British general election campaign in 2024.

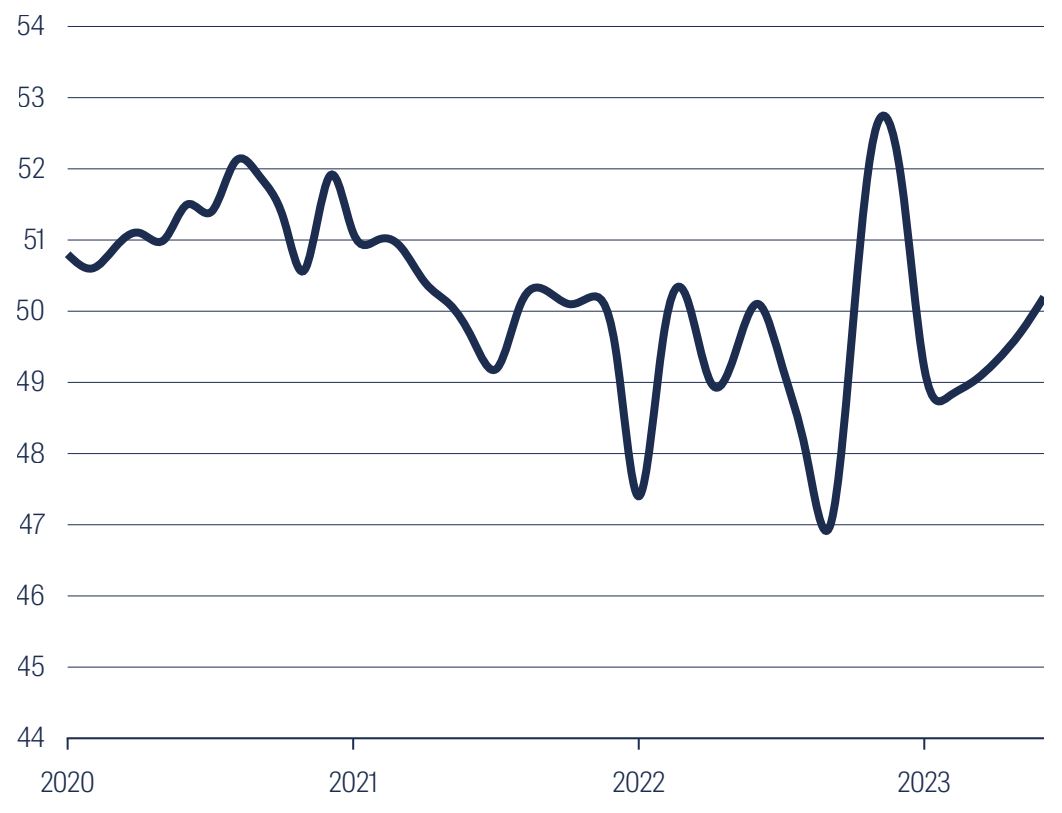

China Industrial activity

One of the last major economies to re-open post COVID-19 was China. The eagerly anticipated economic rebound has been short-lived and my seven meetings with Chinese infrastructure companies reflected this challenging backdrop.

Bustling Hong Kong

Chinese city-gas distributors have the right to distribute gas on a project-by-project level, granted by municipal governments. With industrial users being the largest customer group by volume, the gas utility sector has provided a way for investors to gain exposure to the industrialisation of the Chinese economy. This manifested itself in double-digit year-on-year gas volume growth over the past decade. However a range of factors – namely prolonged disruption from COVID-19 lockdowns, a softening domestic property construction market and, more recently, weak manufacturing demand from the US and domestically – have represented severe headwinds to China’s gas volume growth in 2023.

Pleasingly, nationwide gas volume growth has showed signs of acceleration in recent months. Further, companies are cautiously optimistic about their progress in passing through higher gas costs to residential customers, and about their ability to connect existing properties (previously without gas connections) as the number of new properties being built normalises to more sustainable levels.

China Manufacturing PMI

Source: Bloomberg, FSI as at 30 September 2023.

PMI = Purchasing Managers' Index, a monthly indicator of economic activity. A PMI reading over 50 indicates growth or expansion of the manufacturing sector, compared to the previous month

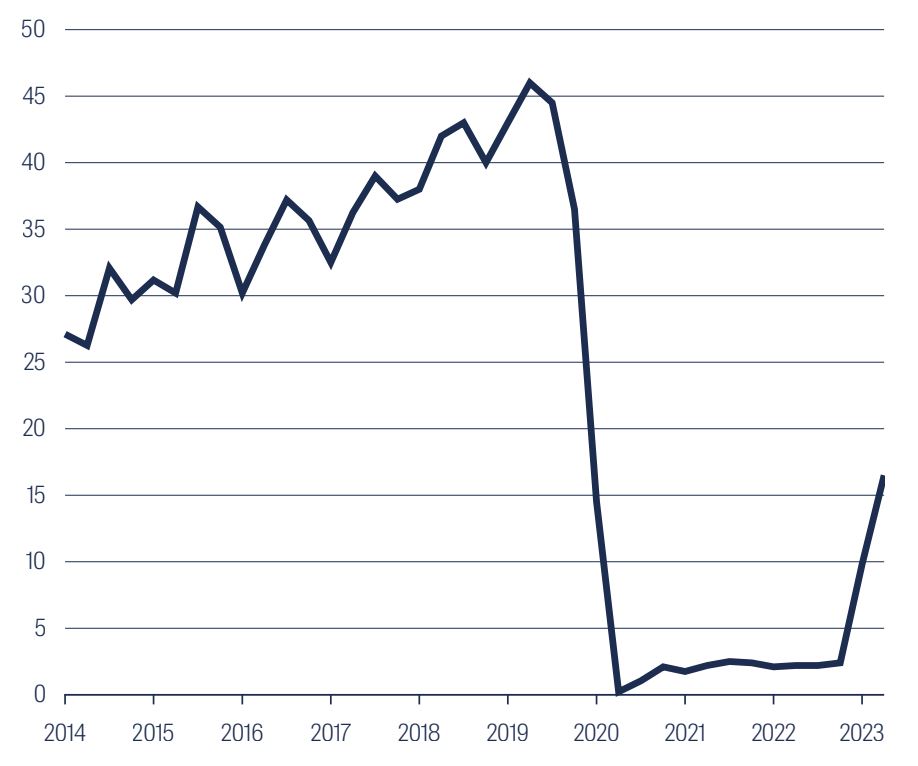

Pre-pandemic, Chinese tourism was a growth driver for airports and retail globally. While there have been a number of reasons for the slow paced return of Chinese tourists, my recent trip provided insight on another issue: limited country-to-country bilateral rights. As European airlines avoid flying over Russian airspace on their way to China, they incur extra costs which they believe place them at a competitive disadvantage to Chinese airlines. As governments work through these issues with their flag carriers, it is slowing the reversion of aircraft capacity back to pre-pandemic levels.

China Outbound Tourists (per month, 000s)

Source: Bloomberg, FSI as at 30 June 2023.

Conclusion

Substantial investment opportunity exists for renewables generation and T&D-focused utilities. However, participants are starting to encounter more challenges in execution. China’s economy is reopening, and outbound tourism from that country is returning. We believe there are positive medium-term tailwinds for Global Listed Infrastructure demand, despite the need to work through near-term challenges.

1 Capital expenditure

2 Power purchase agreements

3 Megawatt hour

4 UK Government Contracts for Difference scheme

Important Information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should consider, with the assistance of a financial advisor, your individual investment needs, objectives and financial situation.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. To the extent this material contains any measurements or data related to environmental, social and governance (ESG) factors, these measurements or data are estimates based on information sourced by the relevant investment team from third parties including portfolio companies and such information may ultimately prove to be inaccurate. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material and we do not undertake to update it in future if circumstances change.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

To the extent this material contains any ESG related commitments or targets, such commitments or targets are current as at the date of publication and have been formulated by the relevant investment team in accordance with either internally developed proprietary frameworks or are otherwise based on the Institutional Investors Group on Climate Change (IIGCC) Paris Aligned Investment Initiative framework. The commitments and targets are based on information and representations made to the relevant investment teams by portfolio companies (which may ultimately prove not be accurate), together with assumptions made by the relevant investment team in relation to future matters such as government policy implementation in ESG and other climate-related areas, enhanced future technology and the actions of portfolio companies (all of which are subject to change over time). As such, achievement of these commitments and targets depend on the ongoing accuracy of such information and representations as well as the realisation of such future matters. Any commitments and targets set out in this material are continuously reviewed by the relevant investment teams and subject to change without notice.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group. Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners, all of which are part of the First Sentier Investors group.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), RQI Investors (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business divisions of First Sentier Investors (Singapore).

- Japan by First Sentier Investors (Japan) Limited, authorised and regulated by the Financial Service Agency (Director of Kanto Local Finance Bureau (Registered Financial Institutions) No.2611)

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167)

- other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

|  |

|---|