- Customers, politicians and shareholders are demanding renewable energy to drive down carbon emissions and grid hardening to limit the impact of hurricanes, storms and wildfires. This investment in mitigation and adaptation is driving up earnings growth.

- Management teams less downbeat than expected, with pricing firm and cost growth moderating. Weather disrupted 1Q earnings but the economy has not deteriorated as much as feared.

- Positive outlook from improved ROEs, load growth from EV demand, tax benefits from IRA, and lower project risk from solar and small nuclear.

Over two weeks we crossed six US states meeting over 70 infrastructure management teams as well as customers and suppliers at three conferences. We visited three corporate head offices, several regulators and toured the country’s largest nuclear power plant.

Earnings on track for 2023

The 2023 earnings outlook for US listed infrastructure companies is broadly on track. While several weather events have disrupted business during the first quarter of 2023, the economy has not deteriorated in the way many had feared.

The pricing environment remains robust, with competition remaining rational. Operating cost inflation has steadied, contractor prices have moderated and fuel prices have declined.

Lower energy prices are working their way into lower customer bills, easing working capital strains at utilities and reducing the risk of adverse political interference. Some supply chain constraints remain, but these are less bad than six months ago. Higher interest costs are now reflected in earnings expectations, with firms focused on lengthening debt maturities.

These factors place listed infrastructure on a solid financial footing, with balance sheets able to support capital investment and dividend growth.

Sophie: We think utilities are well placed to weather the storm that is 2023 (pun intended)

Demand-driven sustainability

From Microsoft to Nucor steel, corporate America’s demand for more sustainable infrastructure is increasing. Why? Because sustainability is popular with customers, and because shareholders want to see carbon emission reduction targets.

Renewable energy projects are increasingly being driven by corporate power purchase agreements or bilateral contracts with utilities. Data centre customers want data storage facilities to be powered by carbon free electricity. Renewable Natural Gas (RNG) providers are signing offtake agreements1 with natural gas utilities who wish to offer low carbon energy to their customers. West Coast municipalities want to use electric garbage trucks in order to reduce emissions. Fast-moving consumer goods (FMCG) firms are driving improvements in plastic recycling levels via polymer plants or automation, advancing the reuse of plastics and supporting a more circular economy2. Oil and gas exploration and production companies are electrifying parts of their operations to reduce emissions. Oil refiners are working on sustainable aviation fuel and renewable diesel.

Andrew: It doesn’t matter if you are in red, blue or purple states — the US is going green

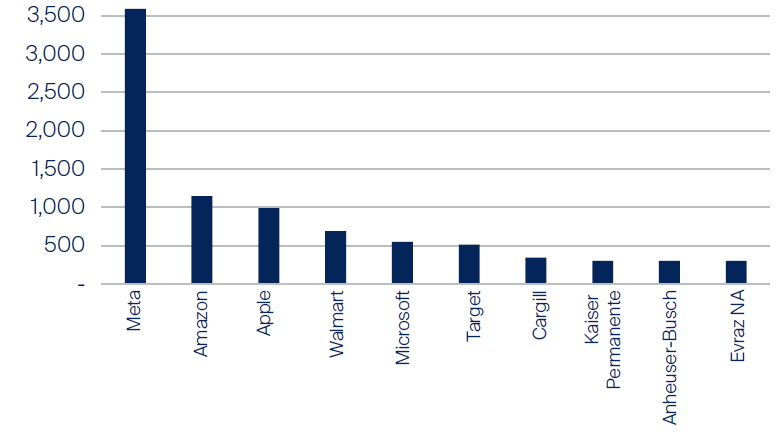

Figure 1: Largest corporate users of solar in US (MW)3

Source: First Sentier Investors, Solar Energy Industries Association. Data as at 30 June 2022.

Regulated utility ROEs to increase in 2023

A key question is whether, in this higher interest rate environment, regulators will increase the allowed Return on Equity (ROE)4 they set for utilities. Many utilities’ current ROEs were set when interest rates were significantly lower. When interest rates were in the 1% - 2% range, many utilities received allowed ROEs of between 8.5% and 9.5%. Now, requests are being submitted by utilities to have their ROEs adjusted higher. With interest rates in the 3% - 4% range, we expect allowed ROEs to push up to between 9.5% and 10.5%5.

While higher customer bills can make regulators reluctant to approve an ROE increase, the sharp decline in energy prices over the past six months is likely to flow through to customers over the next six months. The management teams we spoke to were increasingly confident that they would receive higher ROEs, relative to existing levels. We believe that at least five upcoming rate cases in 2023 will see an increase to the utility’s allowed ROE.

Lower energy prices are already reducing political and regulatory risk in the utility sector; higher regulated ROEs are now set to improve the earnings growth outlook.

Andrew: like Sophie’s mortgage rate, utility allowed ROEs are likely to increase in 2023

Figure 2: Attending investment conference in Orlando, FL.

Source: First Sentier Investors.

EVs impacting late 2020s electricity demand forecasts

We were positively surprised by the number of utilities beginning to incorporate anticipated demand from the electrification of transport into pre-2030 demand forecasts. Many electric utilities are using these higher forecasts to justify planned investments in new generation plants. Duke Energy has forecast that by 2030, Electric Vehicles (EV) will add 2% to retail electricity demand6. Xcel Energy forecasts that EVs will add 0.6% - 0.7% per annum to long term demand for electricity7. DTE Energy estimates that by 2030, 30% of new vehicle sales in Michigan will be electric, and that they will contribute 1%-1.5% to load growth annually8. California-based Edison International is seeing its EV-driven electric demand growth being brought forward9.

We believe utilities are still being conservative in their EV demand forecasts, as we approach the inevitable tipping point from cost parity and the aggressive build-out of charging infrastructure. Post-2030, utility load growth is likely to accelerate significantly in order to cope with EV demand. This will require substantial investment by utilities, not only in generation assets but also in distribution networks which will need to be significantly upgraded. The future is electric and it is arriving now.

Sophie: Have you met an EV owner who doesn’t love their car?

Figure 3: Visiting Duke Energy’s headquarters in Charlotte, NC.

Source: First Sentier Investors.

Climate adaption investment

The reality of climate change causing more frequent severe weather events is leading to a consensus among politicians, regulators and utilities that additional investment is needed to stabilise, harden and increase the resilience of the electric grid. This is increasingly driving new investment in transmission and distribution assets. In California, utilities are taking steps to de-risk the grid from wildfires by investing in sectionalisation devices, wider cross arms, covered conductors and undergrounding. In the south, Texas, Louisiana and Florida utilities are investing in systems that are better equipped to withstand hurricanes, including undergrounding and even portable generators. Winter storms in the mid-west and north-east are driving increased investment in undergrounding. Management at CMS Energy told us “To make the grid more reliable during ice storms, you need to underground”. In the more Republican-leaning states, this investment is seen as economic development rather than climate related. Either way, the reality is clear and the investment is happening.

Sophie: Grid hardening is like designer clothes, the only limiting factor is affordability

Figure 4: 150MW Agave Solar Plant outside Phoenix, AZ.

Source: First Sentier Investors.

IRA to fire up the energy transition from 2024

The energy transition and decarbonisation of electricity generation remains the key theme for utilities. By increasing subsidies for renewables, energy storage and nascent technologies, the Inflation Reduction Act (IRA) will lower the burden on customers for this transition. This enables utilities to increase the scale and scope of their energy transition investments, which we expect to accelerate in 2024. We are encouraged that several utilities are seeing bipartisan support for this decarbonisation both from a climate change and economic development point of view. For example, North Carolina (which has a Republican legislator and Democrat governor) has enacted legislation10 requiring carbon emission reductions of 70% by 2030.

The energy transition is leading to increased capital investments for utilities, ultimately leading to a higher rate base on which they will earn returns. However, as one utility CFO we met stated “Customer bill growth drives the pace of energy transition”.

Andrew: Green is the new black

Nuclear renaissance

The amount of electricity generated by nuclear in the US peaked in 2012, powered by 104 units11. Over the past decade, the country has retired 12 nuclear power units as operating costs increased, while at the same time renewables drove down electricity prices. State-based capacity mechanisms, and now the IRA, have effectively underwritten nuclear power plants by (finally) recognising that they produce 50% of the US’ carbon free electricity12. The next 12 months will see the first new nuclear reactors enter service in the US since 1996. Nuclear power units in the US are 42 years old, on average13.

Going forward, the utility industry is working toward deploying the next generation of nuclear power, Small Modular Reactors (SMRs). SMRs are smaller, with capacity between 75MW and 300MW, compared to traditional nuclear units with capacity between 1,000MW and 1,300MW14. They will be built in centralised factories and then assembled on site, significantly reducing build costs and execution risk. The nuclear experts we spoke to on this trip believe this technology will be operational by the mid-2030s. Nuclear power is the only carbon free electricity source that provides baseload capacity to a system that is increasingly dominated by non-dispatchable, highly variable solar and wind. In addition, nuclear units have the potential to produce material amounts of hydrogen (another carbon-free fuel source) over time.

Andrew: We love nuclear and orange hardhats!

Figure 5: Tour of largest nuclear power plant in US: Palo Verde, AZ.

Source: Palo Verde Generating Station and First Sentier Investors.

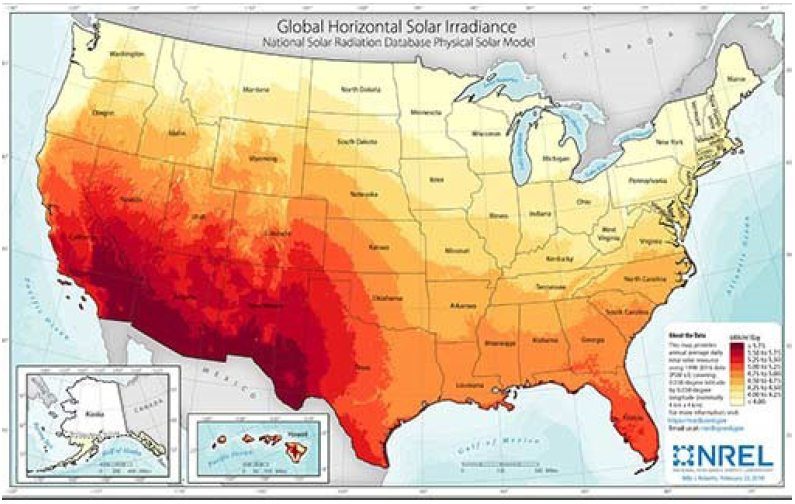

Solar getting its sizzle back

In our travels we visited three of the five largest solar states in the US — Florida, North Carolina and Arizona. In the majority of US states, solar is the lowest cost generation source. Despite regulatory and supply chain problems in 2022, solar still accounted for 50% of all new generation in the US15. The decline in battery costs and IRA subsidy switch from ITC16 to PTC17 will only enhance solar’s status as the leading renewable resource. Utilities in jurisdictions with strong solar resources can decarbonise their generation fleets at a quicker pace, owing to the lower impact on customer bills. Solar also has the advantage of low construction risk. To quote one utility CEO “Building solar farms is like building Lego”.

Andrew: We see little doubt that solar is going to be a must have for years to come, just like a Harry Styles album for Sophie.

Figure 6: US solar resource

Source: NREL.

Energy midstream exporting its way to growth

While utilities and railroads are benefiting from US onshoring18, North American energy midstream growth is being driven by the exporting of natural gas, refined oil, NGLs19 and LPG20. As Russia, China and Iran seek to create a multipolar world order and reduce engagement with the developed world, North America’s abundance of hydrocarbons sees it expanding its role in global energy markets. New investment in the energy midstream sector is mostly focused on export opportunities combined with higher demand from utilities for new gas fired power plants (to replace old coal plants).

Despite spiking natural gas prices in late 2022, political and commercial interest in building new pipelines remains low, reducing the risk of expensive new projects. The only place we see greenfield21 energy midstream projects are in Texas, Louisiana and Oklahoma. Most investments are brownfield22 expansions of existing midstream facilities which have the benefit of lower costs, less approval requirements and fewer NIMBY23 issues.

Sophie: Not wanting to be caught napping (like Andrew on a train or plane), midstream companies are expanding their natural gas infrastructure to capture growing export demand.

Digital infrastructure

Wireless towers, data centers, small cells and fiber are the infrastructure that enables the digital economy. With the 5G rollout from the big 3 US carriers about 50% complete, there appears to be a slowdown in 2023 with expectations of a pick-up again in 202424. Conversations with management indicated that 5G is suffering from the absence of a compelling customer or industrial use requiring greater network investment at present. As a wireless tower CFO stated “Lack of a true ‘must have’ 5G application means carriers don’t need to spend”. Demand for small cells appears to be increasing in 2023 while data centers seem to have escaped the cutbacks seen across much of the technology sector.

Andrew: Sophie cannot wait for 5G rollout to be completed so her TikTok algorithm can load even faster

Fun facts from the road

In 2022, there were 163 physical attacks on the US power grid, an increase of 77% from the prior year25. These attacks were due to a mix of vandalism, terrorism and criminal activity.

One waste company we met with said it is cheaper for them to hire an MBA into a finance role than a truck driver in Houston.

A North American E&P company we met noted that at its oil drilling rigs, 7 out of 8 new hires do not last longer than one month.

A uranium pellet the size of a gummy bear can be used to generate the same amount of energy as 1 ton of coal, 149 gallons of oil or 17,000 cubic feet of natural gas26.

US airports and airlines were very full, but great to see improved retail offerings post COVID at many airports.

Sydney Airport duty free was out of stock of many different types of whisky. Unprecedented.

Andrew did more shopping than Sophie (by a landslide).

Footnotes

1 Contracts between a natural gas producer and a buyer that specifies the terms of sale for a predetermined amount of natural gas over a specified period of time.

2 An economic system that aims to minimise waste and maximise the use of resources by keeping materials and products in use for as long as possible.

3 For illustrative purposes only. Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

4 Return On Equity is a measure of profitability for utilities. A high ROE generally indicates that the utility is generating a strong profit, compared to the amount of equity invested, while a low ROE suggests the opposite.

5 Source: Company reports, First Sentier Investors

6 Source: Duke Energy

7 Source: Xcel Energy

8 Source: DTE Energy

9 Source: Edison International

10 House Bill 951

11 Source: US Energy Information Administration (EIA)

12 Source: US Energy Information Administration (EIA)

13 Source: US Energy Information Administration (EIA)

14 Source: International Atomic Energy Agency (IAEA)

15 Source: US Energy Information Administration (EIA)

16 Investment Tax Credit

17 Production Tax Credit

18 Companies moving production or business processes from overseas to within their home country.

19 Natural Gas Liquids

20 Liquefied Petroleum Gas

21 Land that has yet to be developed

22 Land that has previously been built on

23 “Not In My Back Yard”: opposition by residents to proposed developments in their local area.

24 Source: Company reports, First Sentier Investors

25 Source: Bloomberg

26 Source: Pinnacle West

Important information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure. Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication but the information contained in the material may be subject to change thereafter without notice. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward-looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Investors.

Selling restrictions

Not all First Sentier Investors products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Investors in order to comply with local laws or regulatory requirements in such country.

This material is intended for ‘professional clients’ (as defined by the UK Financial Conduct Authority, or under MiFID II), ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) or Financial Markets Conduct Act 2013 (New Zealand) and ‘professional’ and ‘institutional’ investors as may be defined in the jurisdiction in which the material is received, including Hong Kong, Singapore, Japan, and the United States, and should not be relied upon by or be passed to other persons.

The First Sentier Investors funds referenced in these materials are not registered for sale in the United States and this document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Investors.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors is a business name of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) is a business division of First Sentier Investors (Singapore).

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167).

- other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

|  |

|---|