Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreStewart Investors manage investment portfolios on behalf of our clients over the long term and have held shares in some companies for over 20 years. They launched their first investment strategy in 1988.

Discover more

A monthly review and outlook of the Asian Quality Bond market.

Market review - as at January 2022

Asian credit started off 2022 with negative returns, as US Treasury yields rose and as deteriorating investor sentiment saw spreads widen. Performance was particularly poor in the first half of the month, although a rebound later helped limit losses. The JACI Investment Grade Index declined by 1.88% in the month as a whole.

Strong employment data and quickening inflation exerted upward pressure on US Treasury yields. Headline CPI has risen to an annual rate of 7.0%, the highest level in nearly 40 years. Consequently, by month end five interest rate increases in the US had been priced in to markets; a more aggressive tightening cycle than had previously been anticipated.

At the same time, ongoing concerns of a slowdown in Chinese growth weighed on sentiment. The country’s ‘zero COVID’ tolerance policy could hamper activity levels as authorities try and limit the spread of the virus.

Following a relatively quiet December, January started off with plenty of new issuance, although volatility in rates and spreads saw new issuance dry up as the month progressed. In some cases, rising debt costs prompted issuers to delay offers, particularly if they were required to offer sizeable concessions to attract demand.

Notable new issues included Indian conglomerate Reliance Industries. The BBB rated company raised US$3 billion in a multi-tranche deal. Demand for the new securities was quite firm, with order books more than two times over-subscribed. Other Indian issuers that came to market included State Bank of India and Indian Railway Finance. In Hong Kong, various issuers came to market including Hong Kong Telecom, Link REIT and Hong Kong Airport Authority. The latter raised US$4 billion in a multitranche deal that was offered with a new issue premium over comparable bonds on the secondary market.

Korean firms to complete deals over the month included Korea National Oil and Exim Bank of Korea, which raised US$1.5 billion and US$3 billion, respectively. Both are state-owned entities. Woori Bank, Shinhan Card, and Hanhwa Life were among other Korean issuers that came to market. Elsewhere, China Cinda Asset Management finally sold new bonds – volatility in the asset management space had previously been too high following the Huarong saga. The company completed a US$1 billion deal, which was well supported — the order book was more than four times covered.

Performance review

The First Sentior Asian Quality Bond Fund returned -2.06% for the month of January on a net-of-fees SGD term.

The negative return was largely due to sharp decline in Shimao bond prices as sentiments in China Property space remains weak.

On a relative basis, the fund underperformed the index largely due to our overweight in Shimao. However, our underweight in Indonesia and underweight US rates helped to offset some of the underperformance.

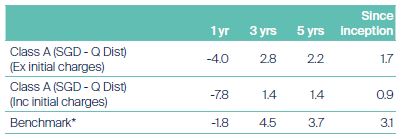

Annualised performance in SGD (%)1

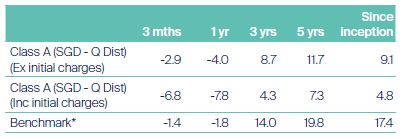

Cumulative performance in SGD (%)1

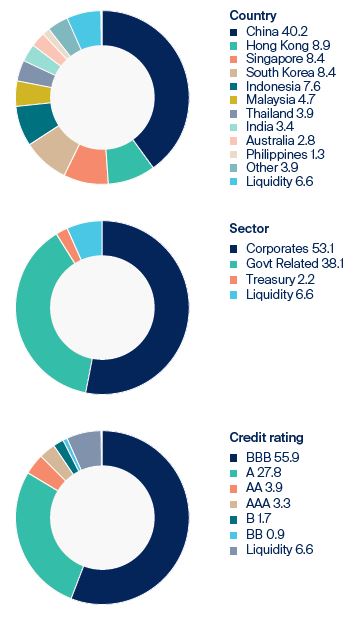

Asset allocation (%)1

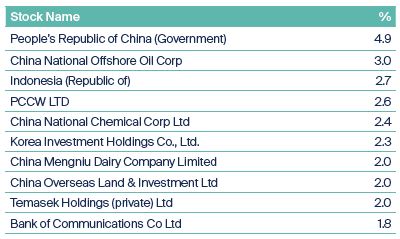

Top 10 holdings (%)1

* The benchmark displayed is the J.P Morgan JACI Investment Grade Index (SGD Index) (Hedged to SGD).

1 Source: Lipper, First Sentier Investors. Single pricing basis with net income reinvested. Data as at 31 January 2022. The First Sentier Asian Quality Bond Fund inception date: 1 November 2016.

Fund positioning

We continued to reduce the Fund’s exposure to the Chinese property sector, through sales in China Jinmao, Vanke, and Country Garden.

On the buy side, long-dated Baba securities were added to the portfolio, following higher US Treasury yields and widening spreads. The ‘all-in’ yield looked more attractive given the credit ratings. We also increased exposure to long-dated bonds issued by Sinopec.

Other excess cash was invested in new issues including Reliance Industries, Hong Kong Airport Authority, Hong Kong Telecom, and Link REIT.

Q1 2022 investment outlook

Despite the ongoing concerns around the COVID Omicron variant dominating the headline news, we believe the key driver of markets as we head into 2022 will be monetary policies normalisation led by the US Fed, followed by the ECB. After all, Fed Chairman Jerome Powell has all but turned hawkish, dropping the “transitory” stance on inflation, which has remained stubbornly at elevated levels. While we do not expect the Fed to move too aggressively in terms of rate hikes, the risk is for them to finally admit they have been behind the curve, should inflation prints stay high over the course of the New Year. Given the lofty valuations of the US equity market along with tight credit spreads especially in US investment grade bonds, we maintain our cautious stance towards risky assets as we move away from ultra-easy monetary conditions. We would also keep a close eye on Chinese government’s policies on the property and technology sectors as these would affect sentiments in the Asian credit markets.

US inflation has been hovering around levels not seen before for the past three decades. The US Fed has for months maintained that high inflation is transitory, as they believed supply chain disruption has been the main cause for higher prices and they expect the bottleneck to ease as economy return to normalcy. It is unfathomable that they have been oblivious to the impact of higher wages and a strong domestic demand, both of which have and will likely continue to exert upward pressure on prices. As real interest rates are now deeply negative, the US Fed now has little choice but to hike rates in 2022 in order to uphold their credibility. Expectation is for them to hike 3-4 times in the New Year, which will bring the Fed fund rate to around 1%, a relatively benign hiking pace when put into context with the terminal rate of around 2.25- 2.5% achieved during the previous hiking cycle. Interestingly, we observed that despite the high inflation print and a heightened rate hike expectations, the 10-year Treasury yield has remained below 1.5%. We believe while the Omicron variant could have kept yields low in recent weeks, the market looking beyond the current high inflation and pricing in slower growth after the rate hike is another explanation for the low treasury yields as the yield curve continues to flatten. While not our base case, US economy heading into stagflation, something which has not happened for decades, cannot be totally ruled out.

While Bank of Korea has started hiking policy rate and Monetary Authority of Singapore has moved to a tightening stance, central banks over in Asia are not pressured to move too quickly as inflation remains benign as the region did not see as strong a rebound in domestic demand when compared to the advanced economies. Countries like India and Indonesia, both of which suffered from previous episodes of Fed’s tightening and taper are now in much better shape. India has recovered strongly from a dire COVID hit spell and look set to maintain its investment grade rating, while Indonesia has also benefitted strongly amid higher commodity prices which has helped improved its balance of payment fundamentals as it is a major exporter of coal and crude palm oil. EMD as an asset class will remain volatile amid a Fed rate hike cycle and hence spreads for Indonesia and Philippines sovereign and quasi bonds may face some volatility. Nevertheless, we do see any prolonged weakness as a buying opportunity as these two countries are low beta within the EMD space.

While a Fed rate hike cycle is usually accompanied by a period of continued USD strength and hence Asian currencies weakness, that trend could be quickly reversed should the ECB start to tighten its monetary conditions amid rising inflation in Eurozone, reaching levels not seen for decades. Furthermore, should expectations of slower growth gain momentum, bullish dollar positioning could further be pared down. Rate hikes by Asian central banks may also help to ease some depreciating pressure on their currencies. The Asian dollar index has gained more than 3% in 2021. Barring the Fed entering into an aggressive hiking cycle, further upside for the dollar is likely to be more gradual.

Despite facing numerous challenges throughout 2021, which include the Huarong saga, clampdown on China’s technology sector and the ongoing liquidity crisis in the property sector, Asian credits’ valuation (excluding property) are currently trading at close to historical tight. This leaves us with little buffer to cushion against the imminent rate hike by the US Fed and hence total return’s expectation for 2022 needs to be tapered.

While we do not expect a U-turn in the Chinese government’s policies around the tightening of regulations for the technology sector and deleveraging of the property sectors, any softening in tone or steps to support growth should be closely watched as this will likely bring about a change in sentiments which has clouded the market for many months. We maintain that the Chinese property market is currently facing a liquidity crisis, not a solvency crisis. The key question is how much longer can China tolerate the pain? After all, the property sector accounts for at least 20% of GDP growth and has indirect impact on other sectors such as steel and cement. More importantly, the prospect of significant job losses and social unrest as a result of a collapse in property market can never be underestimated. Based on current valuation, the property sector is pricing in a default rate of close to 40%, which suggests the market is trading on fear rather than on fundamentals. Nevertheless, with numerous bond maturities coming up in the first quarter 2022, the sector can remain under pressure in the months ahead.

While the concerns over China remains, there are some bright spots within Asian credits. India’s economy has recovered strongly after being ravaged for months by COVID. This led to Moody’s changing the sovereign’s outlook from negative to stable. This has all but removed the downgrade risk to high yield for many India investment grade credits. Similarly, Indonesia has recovered strongly from the pandemic and has been benefitting from the high commodity prices, being a major commodity exporter. The stronger balance of payment positions, a benign inflation and with foreign investors holding of the local currency government bond at historical low means that Indonesia will likely weather the upcoming Fed rate hike much better than the previous episodes.

The supply picture looks highly favorable for Asian credits in 2022 with gross supply likely to remain little change from 2021. In fact, we believe some of next year’s maturities could already been pre-funded to take advantage of the current low rates in anticipation of the Fed rate hikes. India and Indonesia corporates are likely to benefit from the continued improvement in onshore funding and hence have lesser need for USD issuance. Chinese high yield sector remains shut amid the high double-digit yields many issuers are trading at. Overall, we believe demand will continue to dwarf supply especially should we get a boost from a change in sentiments towards China.

In conclusion, we do not expect the Omicron or any subsequent variant to derail economic recovery in the 1st half of 2022. The determination by many countries to “live with COVID” remains strong after almost two years of fighting the pandemic. Monetary policies by the Fed and the ECB taking over COVID as the key market driver are likely as we head into 2022. China’s policies will also have an important bearing on Asian credits’ performance. Against the above mentioned backdrop, we bring along a cautious stance as we move into the new year, while patiently await for opportunities to emerge.

Source : Company data, First Sentier Investors, as of 31 January 2022

Important Information

This document is prepared by First Sentier Investors (Singapore) (“FSI”) (Co. Reg No. 196900420D.) whose views and opinions expressed or implied in the document are subject to change without notice. FSI accepts no liability whatsoever for any loss, whether direct or indirect, arising from any use of or reliance on this document. This document is published for general information and general circulation only and does not have any regard to the specific investment objectives, financial situation and particular needs of any specific person who may receive this document. Investors may wish to seek advice from a financial adviser and should read the Prospectus, available from First Sentier Investors (Singapore) or any of our Distributors before deciding to subscribe for the Fund. In the event that the investor chooses not to seek advice from a financial adviser, he should consider carefully whether the Fund in question is suitable for him. Past performance of the Fund or the Manager, and any economic and market trends or forecast, are not indicative of the future or likely performance of the Fund or the Manager. The value of units in the Fund, and any income accruing to the units from the Fund, may fall as well as rise. Investors should note that their investment is exposed to fluctuations in exchange rates if the base currency of the Fund and/or underlying investment is different from the currency of your investment. Units are not available to US persons.

Applications for units of the Fund must be made on the application forms accompanying the prospectus. Investments in unit trusts are not obligations of, deposits in, or guaranteed or insured by First Sentier Investors (Singapore), and are subject to risks, including the possible loss of the principal amount invested.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of FSI’s portfolios at a certain point in time, and the holdings may change over time.

In the event of discrepancies between the marketing materials and the Prospectus, the Prospectus shall prevail.

In Singapore, this document is issued by First Sentier Investors (Singapore) whose company registration number is 196900420D. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) is a business division of First Sentier Investors (Singapore).

First Sentier Investors (Singapore) is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions..

MUFG and its subsidiaries are not responsible for any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

|  |

|---|