Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreStewart Investors manage investment portfolios on behalf of our clients over the long term and have held shares in some companies for over 20 years. They launched their first investment strategy in 1988.

Discover more

Please read the following important information for First Sentier Asian Quality Bond Fund

• The Fund invests primarily in debt securities of governments or quasi-government organization in Asia and/or issuers organised, headquartered or having their primary business operations in Asia.

• The Fund’s investments may be concentrated in a single, small number of countries or specific region which may have higher volatility or greater loss of capital than more diversified portfolios.

• The Fund invests in emerging markets which may have increased risks than developed markets including liquidity risk, currency risk/control, political and economic uncertainties, high degree of volatility, settlement risk and custody risk.

• The Fund invests in sovereign debt securities which are exposed to political, social and economic risks. The Fund may also expose to RMB currency and conversion risk.

• The Fund invests in debts or fixed income securities which may be subject to credit, interest rate, currency and credit rating reliability risks which would negatively affect its value. Investment grade securities may be subject to risk of being downgraded and the value of the Fund may be adversely affected. The Fund may invest in below investment grade, unrated debt securities which exposes to greater volatility risk, default risk and price changes due to change in the issuer's creditworthiness.

• The Fund may use FDIs for efficient portfolio management purposes, which may subject the Fund to additional liquidity, valuation, counterparty and over the counter transaction risks.

• For certain share classes, the Fund may at its discretion pay dividend out of capital or pay fees and expenses out of capital to increase distributable income and effectively a distribution out of capital. This amounts to a return or withdrawal of your original investment or from any capital gains attributable to that, and may result in an immediate decrease of NAV per share.

• It is possible that a part or entire value of your investment could be lost. You should not base your investment decision solely on this document. Please read the offering document including risk factors for details.

A monthly review and outlook of the Asian Quality Bond market.

Market review - as at October 2021

Credit spreads tightened during the month but it was not enough to offset the rise in US Treasury yields. As a result, the JACI Investment Grade Index declined in value by 0.31%.

Volatility in the sector picked up, partly reflecting concern over leverage in the Chinese high yield property sector. Whilst not affecting investment grade issuers directly, these concerns eroded sentiment towards the market as a whole, particularly for Chinese issuers.

There were some separate unwelcome developments with other Chinese issuers too. Online retailer Meituan was fined by regulators, who cited breaches of anti-competition guidelines. The government also said it will increase scrutiny of the internet sector; officials are half way through a six-month campaign to address perceived problems with digital firms, including sub-standard data security practices. Finally, the Federal Communications Commission in the US banned China Telecom from operating in America, alleging the company does not operate autonomously from the Chinese government. This move threatened to reignite tensions between the world’s two largest economies, which could have broader implications for sentiment towards Chinese issuers in other industry sectors.

The increase in Treasury yields initially led to a sell-off in longer-dated bonds, particularly sovereign issues in Indonesia and the Philippines, which are typically quite sensitive to changes in interest rates. That said, valuations improved towards month end as higher Treasury yields and wider spreads made all-in yields more enticing. Indonesian bonds, in particular, were also buoyed by robust flows into emerging market hard currency exchange traded funds, and higher commodity prices that benefit export revenues.

Highlights on the new issuance front included US$4 billion of new Chinese sovereign bonds. The order book was six times over-subscribed, underlining the extent of demand for Chinese government-issued debt. South Korea also issued US$500 million of new sovereign bonds. Among corporates, Taiwanese chipmaker TSMC raised US$4.5 billion in a four-tranche deal, including an inaugural issue of 20- and 30-year securities. The scarcity of long-dated bonds in Asia meant these issues were well supported by investors. ICBC Financial Leasing and Indofood were among other companies to complete sizeable issues over the month. In general, demand for these deals was quite strong, particularly in high quality names that offer good diversification from Chinese exposures.

Performance review

The First Sentier Asian Quality Bond Fund returned -0.57% for the month of October on a net-of-fees basis.

The negative return was largely due to rising US Treasury yields. The modest tightening of Asian investment grade spread was not enough to offset this move.

On a relative basis, the fund underperformed the index largely due to our overweight in 2 Chinese property developers SHIMAO and COGARD which witnessed some spread widening amid the sharp sell-off in the high yield space.

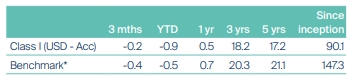

Cumulative performance in USD (%) 1

Calendar year performance in USD (%) 1

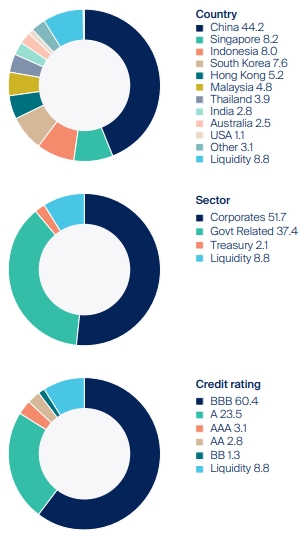

Asset allocation (%) 1

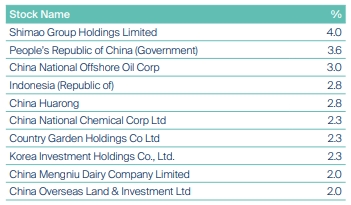

Top 10 holdings (%) 1

Performance is based on First Sentier Asian Quality Bond Fund Class I (USD - Acc) is the non-dividend distributing class of the Fund, the performance quoted are based on USD total return (non-dividend distribution).

This Fund is a sub fund of Ireland domiciled First Sentier Investors Global Umbrella Fund Plc.

* The benchmark displayed is the J.P. Morgan JACI Investment Grade Index.

1 Source: Lipper & First Sentier Investors, Nav-Nav (USD total return) as at 31 October 2021. Allocation percentage is rounded to the nearest one decimal place and the total allocation percentage may not add up to 100%. Fund inception date: 14 July 2003.

Fund positioning

We continued to increase diversification in the portfolio, deploying inflows and excess cash into various issuers in different markets. The Fund bought KB Securities and Hana Bank in South Korea, for example, as well as Indonesian investment grade corporates Tower Bersama and Indofood. The Fund also participated in the issuance of new Chinese sovereign bonds, which were attractively priced relative to comparable bonds trading on the secondary market.

On the sell side, we reduced the Fund’s investment in Indonesian sovereign bonds, with a view of re-establishing the exposure when all-in yields are higher. We are anticipating a further increase in US Treasury yields, which could feed through to a sell-off in emerging market hard currency assets. Exposure to Haohua was also reduced over the month, locking in profits from recent favorable performance.

Finally, we increased the scale of the Fund’s existing short duration position in US rates. This strategy has aided relative performance recently as yields have risen, but we believe persistent inflationary pressures will continue to push yields higher.

Q4 2021 investment outlook

As we navigate into the last quarter of a tumultuous year there are some signs of optimism emerging, despite a backdrop that remains highly uncertain. Countries that have been suffering intensely from Covid-19 have seen daily cases decline sharply as community immunity has increased. Vaccination rates around the world have also risen significantly and we now expect more countries to achieve the critical 75% vaccination rate as early as the first half of 2022.

Economically, recent data releases in the US and China indicate that global growth momentum has slowed as the Covid Delta variant has spread. Nevertheless, after close to two years mired in a Covid world, there has been increasing commitment from many countries around the world to continue re-opening their economies. Progress with vaccinations in Asia has been particularly encouraging and many countries in the region are expected to achieve the all-important 75% vaccination rate by the end of this year. Even the worst hit countries, including India and Indonesia, are on track to reach the 75% threshold by the end of March 2022, which is much earlier than earlier projections. Moreover, while the Delta variant is more contagious than earlier forms of Covid-19, the symptoms are typically milder as the virus has mutated. Higher vaccination rates, a build-up of natural immunity in the community and the mutation of the virus into weaker forms suggests we could move from a pandemic towards an endemic phase in the next six to nine months.

As the trajectory of the Covid situation continues to point towards an improvement, major central banks led by the US Federal Reserve and the Bank of England seem likely to start withdrawing their highly accommodative monetary policies. The Federal Reserve all but confirmed it will start tapering its bond purchase program in November, and will likely hike policy rates in 2022 if economic growth and labor markets continue to improve. Nonetheless, monetary conditions are expected to remain largely accommodative barring a sharp rise in longer-term inflation expectations. That would challenge the Federal Reserve’s definition of ‘transitory’ inflation. How long can US policymakers allow inflation to stay at current elevated levels? Supply chain disruptions aside, could structural changes to business’ cost base lead to a more sustained level of higher inflation? Will pent-up demand from consumers further propel prices higher? As the world has not experienced any meaningful inflation since after the Global Financial Crisis in 2009, the market may have underestimated the effect of a prolonged period of heightened inflation.

The Bank of England has taken things a step further, suggesting that interest rates could be raised before the UK’s bond purchase program is complete. We see these kinds of moves as necessary; ultimately, keeping policy rates at very low levels while continuing with aggressive quantitative easing will affect central banks’ ability to respond to future crises. We have always questioned the effectiveness of monetary policy to tackle problems caused by a virus. We also believe several years of money printing has sowed the seeds for a bigger problem we will have to deal with in the future; the magnitude of this future predicament could dwarf the effects of the Covid pandemic.

We were reassured by developments with China Huarong Asset Management during the September quarter, but the same kind of government support does not seem to be forthcoming for Evergrande Group. Consequently we are concerned about the potential contagion effect on other property developers and their ability to raise funds, particularly in offshore markets. This is being reflected in valuations — bonds issued by many B-rated developers are now trading on high double-digit yields. Some investment grade Chinese property names including Shimao and Cogard could come under pressure if the Evergrande situation deteriorates, although we remain comfortable at this stage with the credit profile of these two issuers. With the property sector accounting for at least 20% of China’s GDP growth, we do not think Beijing can afford to let this sector sink deeper into a liquidity crunch and risk a run on property developers. Accordingly we expect to see some targeted easing of credit access, allowing developers to refinance upcoming debt maturity such that the construction process can continue. On a more positive note, the ‘3 Red Lines’ policy that was put in place by the Chinese government in 2020 has already helped to improve the debt profile of the property sector, which augurs well for longer-term stability. While deleveraging looks set to continue, the government still has flexibility to fine-tune policies if other developers show signs of financial duress.

Following lackluster returns in the September quarter, Asian credit markets are still showing negative total returns in the calendar year to date. Investment grade issuers have outperformed their higher yielding peers this year due to their more resilient and stable credit profile. With the Huarong issue seemingly resolved, we believe investment grade spreads will remain fairly well supported. The key risk is that the US Federal Reserve increases borrowing costs more quickly and/or more significantly than the market expects. In that case, sentiment towards investment grade credit could be adversely impacted given all-in yields remain close to historical lows.

Finally, against the backdrop of likely tapering of bond purchases by the US Federal Reserve and the potential for interest rate hikes in 2022, the US dollar is expected to trade strongly against Asian currencies. Should expectations of monetary policy tightening in the US be pared back, however, or if Asian central banks embark on a monetary policy tightening path, the outlook for Asian currencies would be much brighter. How quickly Asian economies get the Covid pandemic under control will also likely have a meaningful influence on currencies’ performance in the months ahead.

Source : Company data, First Sentier Investors, as of end of October 2021

Important Information

Investment involves risks, past performance is not a guide to future performance. Refer to the offering documents of the respective funds for details, including risk factors. The information contained within this document has been obtained from sources that First Sentier Investors (“FSI”) believes to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy or completeness of the information. Neither FSI, nor any of its associates, nor any director, officer or employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this. It does not constitute investment advice and should not be used as the basis of any investment decision, nor should it be treated as a recommendation for any investment. The information in this document may not be edited and/or reproduced in whole or in part without the prior consent of FSI.

This document is issued by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong. First Sentier Investors is a business name of First Sentier Investors (Hong Kong) Limited.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

First Sentier Investors (Hong Kong) Limited is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions.

MUFG and its subsidiaries are not responsible for any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

|  |

|---|