Macro towers will remain at the heart of a modern, mobile data communications network

- Macro towers sit in the sweet spot of mobile network deployment, balancing wide-area coverage with high-speed network capacity.

- We believe they are well suited to serve society’s growing mobile data needs today and in the years to come, especially with new higher-frequency spectrum.

- New direct-to-smartphone satellite fleets expand coverage further but are not expected to provide the same broadband-level user experience as towers

This paper asserts that macro towers will remain at the heart of a modern, mobile data communications network despite the continual development of new technologies.

Data communications networks have gone through an extraordinary evolution as society has generated and consumed ever-increasing amounts of data, while shifting to mobile at the expense of fixed. Macro towers have been key enabling assets as network architecture has evolved and mobile data traffic has grown.

Exciting, innovative technologies (such as satellite direct-to-smartphone connectivity for Apple & Android) are announced periodically, raising questions around whether they may adversely affect demand for mobile tower space. The short answer is no, in our opinion. Moreover, we believe current network architecture trends should see the network brought closer to users which will be a tailwind for tower demand.

The rest of this paper explores these views in greater detail.

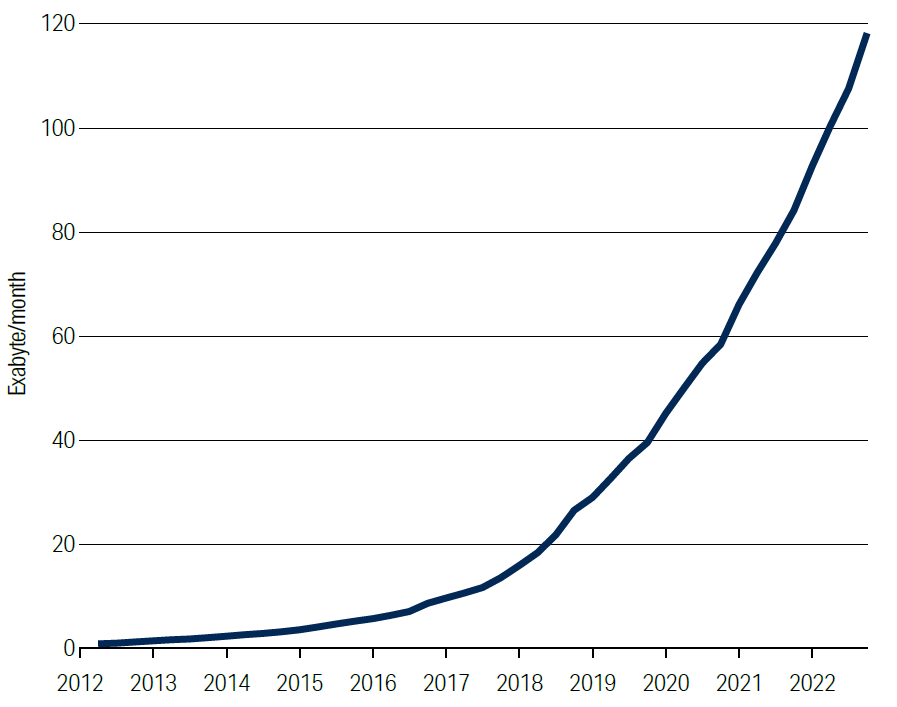

Figure 1. Mobile data traffic

Source: Ericsson Mobility Visualizer, First Sentier Investors as at 31 March 2023.

1 exabyte = 1 billion gigabytes

The continuum of coverage

We would like to introduce the concept of the continuum of coverage. As a person moves through the physical environment they are best served by different communication technologies. Whilst coverage areas for each technology may overlap somewhat, we believe they are complementary to each other, rather than competitive.

Figure 2: your Tower analyst at a CBD/downtown small cell system in Houston

Source: First Sentier Investors

Telecommunication technologies involve a trade-off between capacity (bandwidth or how ‘fast’ a connection is) and coverage (how far the signal travels). If coverage is wide, the wireless signal is spread out over a larger area, typically reducing capacity. Conversely, shorter range coverage should see the highest capacity.

Traditionally, data networking activity was performed in an indoor environment such as a home, workplace or school with a physical wired connection. As the use of smartphones, tablets and laptops grew, that activity evolved wirelessly using Wi-Fi which provides high capacity - albeit at a limited distance of up to 50 metres (or less). Despite the usefulness of Wi-Fi, mobile has served as an increasingly important tool for communication needs as cellular signals began to penetrate buildings and speeds reached broadband-like levels. In fact, network equipment manufacturer Nokia claim that 80% of mobile data now originates from mobile users located indoors1.

As the user moves outside into a dense urban area, their signal may be handed off to the next source of network connection, perhaps a rooftop cell site or, increasingly, a small cell antenna system installed on street lights and other street furniture. Here, the range of coverage is typically up to 200 metres but in some cases can be up to two kilometres.

Once the user reaches a suburban area where people are more widely dispersed, the density of people requiring a wireless connection declines. At this point, users are served by macro towers with coverage of several kilometres or more. Towers occupy the sweet spot of deployment choice. They provide coverage to a large area with sufficient bandwidth capacity, in locations where subscribers predominantly live and work.

Beyond that, as the user moves to rural areas, population density decreases further and coverage becomes sparser. Telecom operators (excluding coverage obligations) need to make commercial decisions around whether there are enough subscribers to justify servicing these areas. Beyond that, in remote and wilderness areas, our user’s only means of mobile communication may be through a (non-smart) satellite phone.

We believe there is no one-size-fits-all solution for wireless network deployment; and that the best solution is a balance of providing the highest bandwidth to the largest number of data users whilst minimising capex and opex. Wi-Fi is acceptable for an indoor environment but only covers a modest area. A small cell covers a greater area than Wi-Fi and provides high capacity which is well suited to a densely populated urban area. However, we estimate that many of them would need to be deployed to cover the area that could be serviced by a single macro tower, making small cells a more expensive choice.

Figure 3: Relative coverage areas of Wi-Fi vs Towers

Source: First Sentier Investors estimates

Actual range depends on other factors including but not limited to power, terrain, buildings

For illustrative purposes

It is tempting to seek the next technology, which can propagate wireless signals further than macro towers. However, we soon begin to trade off coverage for capacity. Experimental aircraft or satellites are many times farther away from the ground than the tower. This materially reduces the bandwidth available at the smartphone, to the extent it is not a competing broadband-speed connection. These solutions likely have a place for remote or wilderness locations where users are scarce.

Stay in your lane

Figure 4: Distance from smartphone to wireless network signal

Over the 15 years that we have researched and invested in the tower sector, a number of novel inventions have promised to provide alternative means of mobile connectivity. However, we believe that none have offered the same benefit of cost/coverage/capacity as towers. Many have since been discontinued; today none, in our view, pose a material competitive threat.

Source: First Sentier Investors estimates as at 31 March 2023

Log-scale

Solar-powered planes or balloons

Proponents of these unmanned systems were typically technology companies seeking to extend internet connectivity towards previously unserved communities – thus increasing the addressable market for their own services. These systems were designed to fly at an altitude of between 15–30 kilometres (km) and stream data connectivity to the ground.

We were sceptical, believing that the long distance between aircraft/balloon and smartphone would compromise the capacity available to the end user. Both of these projects have been quietly discontinued in recent years.

Satellites

Not all satellites are created equal. Earlier GEO2 communications satellites orbit 35,786km above Earth. Ground users require a large satellite dish to send and receive a signal. Once again, the distance between the user and the network source (the satellite) has proved too great, resulting in reduced capacity.

Newer generations (LEO3) have generated much attention for all the right reasons; backed by successful entrepreneurs/founders (Elon Musk’s Starlink, Jeff Bezos’ Kuiper) and the prospect of direct-to-smartphone connections (no need for a satellite dish4 or separate smartphone for Apple5/Globalstar, Qualcomm/Android/Iridium6, AST SpaceMobile or Lynk)7. With credible backers from some of the most innovative companies in telecom and tech, LEO satellites represent a potential threat to towers that deserves to be taken seriously.

Figure 5: Qualcomm’s Android chip requires the user to be outside and point to the sky

Source: Qualcomm as at Jan 6 2023.

However, one constant that is harder to disrupt is the laws of physics (see section below on Inverse square law of electromagnetic radiation). These newer satellite fleets, whilst closer to the ground than legacy fleets, still have orbits in excess of 500km. This distance diminishes the bandwidth that reaches the end user. It does not surprise us that Apple, Qualcomm and T-Mobile are championing an SMS-type service rather than a low-latency, full-service broadband replacement.

Even the US Federal Communications Commission8 has acknowledged the limitations, noting that “these early space communications projects will not provide high-speed broadband from the stratosphere to our phones. But to start, they could deliver low-bandwidth connectivity suitable for emergency calls and texts in remote settings where terrestrial networks do not reach”. Furthermore, the smartphone user needs to be outside, which is at odds with where the majority of data is used.

Figure 6: Trade-off between distance and throughput at the smartphone

Source: First Sentier Investors estimates as at 31 March 2023

Tower: Speedtest Global Index Mobile USA January 2023

Starlink/T-Mobile: Elon Musk 2-4Mbits per cell zone

Apple: Emergency SMS only; Globalstar satellite phone data speed proxy

YouTube/Netflix: Recommended speed for 4K video (15-20Mbps)

While technical details are limited at this point in time and technology may change, Figure 6 illustrates the trade-off between distance and throughput at the user device for the various technologies. The average American mobile user can download at 80Mbps9. As a comparison, the chart also include the recommended connection speeds of popular video streaming services - well in excess of what these direct-to-phone satellite systems plan to offer.

Therefore, we believe that satellite broadband connectivity lies at the end of the continuum of coverage and is unlikely to displace macro towers as the key enabler of mobile networks.

Inverse square law of electromagnetic radiation10

Mobile data networks are built using radios and antenna that generate a wireless signal on the electromagnetic radiation spectrum. Signal strength is inversely proportional to the distance from the source squared. That is, if you double the distance, the power is one-quarter of what it was previously. Given satellites are multiple times farther away from the smartphone than a tower, this law magnifies the reduction in signal strength and thus throughput to the end user.

Heading in the wrong direction

While these new technologies involve deploying wireless signals further away from the user, the structural trend in mobile network deployment is to bring the signal (and equipment) closer to the end user.

The overarching driver behind this is fast-growing mobile data demand rapidly consuming wireless network capacity. Network equipment provider, Ericsson estimate current mobile network data growth in excess of 40% per annum, after growing at greater than 50% for most of the prior decade (Figure 1).

Mobile network operators11 create extra capacity by densifying their cell sites (installing more of them, closer together) and by purchasing more spectrum from regulators.

Densification of cell sites (or “cell splitting”) occurs when a second or third cell site is deployed on a nearby tower to take mobile traffic off a congested cell site. In the United States this benefits tower companies as wireless carriers sign a new lease to collocate on tower space to install another set of radios and antenna on the adjacent site.

Figure 7: Tower and small cell owner, Crown Castle’s view of network densification

Source: Crown Castle Investor Presentation February 2023

At the same time as cell splitting, regulators have been and continue to allocate more spectrum to telcos to facilitate mobile network capacity growth. Prior generations of mobile network technology (2G 3G) were based around low-band/frequency spectrum. As these bands near exhaustion, regulators have been progressively unlocking under-utilised12 mid-high band spectrum for 4G and 5G. These higher frequency bands also enable the higher capacity and lower latency performance benefits of 4G and 5G.

Figure 8: US spectrum allocations have been towards higher frequencies13

Illustration of some US mobile spectrum allocations over time

Source: FCC, First Sentier Investors as at 31 March 2023

Spectrum is allocated/used in bands rather than a point as depicted (for simplicity)

2.5GHz had multiple ownership changes, 2014 depicts material mobile deployment Not exhaustive

Low-band spectrum typically propagates long distances, and is very effective for voice and SMS applications. Mid-band spectrum does not travel as far, while high-band spectrum has the smallest coverage radius, all else being equal. As the newer spectrum is in the mid to high-band range, this has a positive effect on cell site density compared to low-band spectrum as the sites need to be closer together (Figure 9).

Figure 9: Wireless carrier, T-Mobile's, illustration of the coverage radius of different spectrum bands

Source: T-Mobile

Most of the time, mobile network operators deploy new spectrum by adding extra antennas and radios to the towers that they use. In industry parlance, this activity is called an amendment. The monthly tower rent increases to accommodate the extra equipment.

The result of this network deployment activity manifests itself in steady growth in tower revenue over time. In Figure 10, we highlight the three listed US tower companies, American Tower, Crown Castle and SBA Communications as that country has the most established independent tower market with the best industry structure to monetise these demand trends.

Figure 10: US listed towers' domestic revenue

Source: Company reports, First Sentier Investors as at 31 March 2023

Material M&A: AMT 2015, CCI 2013

In the future, we may see scenarios where even greater usage of mid to high-band spectrum drives further cell splitting and deployment on outdoor small cells, which, as described earlier, have shorter radius propagation characteristics than towers.

The deployment of small cells has been challenging in recent years as carriers favour the cost and coverage benefits of macro towers.

Small cells rely on optic fiber in the ground, some of which has not been laid or is not of sufficient quality to serve wireless networking. The zoning, permitting, and construction process is lengthy (leading small cell developer Crown Castle claim 24-36 months) which contributes to carriers leaning towards colocating on an existing tower.

Figure 11: SBA Communications tower in suburban Florida

Source: First Sentier Investors

In years to come, there may be a scenario where small cell systems built today find a niche in network deployment as the macro tower-deployed network capacity is used up and ever higher spectrum frequencies require antennas to be located nearer to smartphone users. Crown Castle and Italian tower company, INWIT, have small cell aspirations and we believe would be well placed to benefit from this.

Conclusion

Smartphone users’ data connectivity needs are met by a range of technologies as they move through the physical environment. Towers have an acceptable trade-off between coverage range and data speeds compared to existing and planned technologies. In fact, as higher frequency spectrum is unlocked, the structural tailwind is for mobile network equipment to be deployed closer to the end user.

Footnotes

1 https://www.nokia.com/networks/mobile-networks/small-cells/

2 Geosynchronous earth orbit

3 Low earth orbit

4 Starlink has multiple satellite product offerings. There is an operational fixed broadband product that offers cable/fiber-level broadband speeds but requires a pizza-box sized dish on the ground or rooftop. In late 2022 they announced a proposed direct-to-smartphone partnership with T-Mobile that intends to connect directly to smartphones

5 Apple announced in September 2022, started US & Canada operations November 2022. Expect to use Globalstar’s 1,414km altitude LEO fleet

6 Qualcomm and Iridium announced satellite-based messaging solution for select Android phones in February 2023

7 For illustrative purposes only. Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

8 Chairwoman Rosenworcel Keynote Address to Mobile World Congress February 2023

9 Megabits per second

10 We are infrastructure investors and not telecom engineers so please excuse our simplification

11 We use the terms mobile network operator, wireless carrier and telecom operator interchangeably for our UK/European, North American and Australian readers

12 As a sign of technological advances and the disruption mobile data & wireless communications has caused to traditional business models, recent US spectrum re-allocations have been away from TV broadcasters (600Mhz) and satellite operators (C-band, 3.7Ghz).

13 This figure excludes millimetre wave high-band spectrum auctions in 24GHz-47GHz ranges

Global listed infrastructure insights

Important Information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should consider, with the assistance of a financial advisor, your individual investment needs, objectives and financial situation.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material and we do not undertake to update it in future if circumstances change.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Group.

About First Sentier Group

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Group, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group. Certain of our investment teams operate under the trading names AlbaCore Capital Group, First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners, all of which are part of the First Sentier Group.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Group, First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Group (registration number 53507290B), First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), RQI Investors (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business names of First Sentier Investors (Singapore).

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, registered with the Securities Exchange Commission (SEC# 801-93167)

- other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

To the extent this material contains any measurements or data related to environmental, social and governance (ESG) factors, these measurements or data are estimates based on information sourced by First Sentier Group from third parties and such information may ultimately prove to be inaccurate.

To the extent this material contains any ESG related commitments or targets, such commitments or targets are current as at the date of publication and have been formulated by First Sentier Group in accordance with either internally developed proprietary frameworks or are otherwise based on external frameworks. The commitments and targets are based on information and representations made by external parties (which may ultimately prove not be accurate), together with assumptions made by First Sentier Group in relation to future matters such as government policy, implementation in ESG and other climate-related areas and, enhanced future technology (all of which are subject to change over time). As such, achievement of these commitments and targets depends on the ongoing accuracy of such information and representations as well as the realisation of such future matters. First Sentier Group will report on progress made towards achieving these targets on an annual basis in its Climate Change Action Plan and other reporting. The commitments and targets set out in this material are continuously reviewed by First Sentier Group and subject to change without notice.

© First Sentier Group