Higher interest rates – how much of a threat are they really to corporate borrowers?

Many investors are questioning how rising interest rates will affect corporate borrowers. Will their financing costs rise significantly and, from a credit investors’ perspective, do higher rates elevate default risk?

Consensus forecasts indicate default rates could rise from current low levels, but a closer look at the data suggests any increase could be relatively modest. The reason is that many corporate borrowers have already locked in low borrowing costs, which should help mitigate the impact of rising interest rates.

All of this is important for credit investors. With fewer companies at risk from credit default than would normally be expected at this stage of a rate hiking cycle, the additional return offered by global credit should remain attractive when compared to comparable government bonds.

Long-dated debt issuance provides some protection

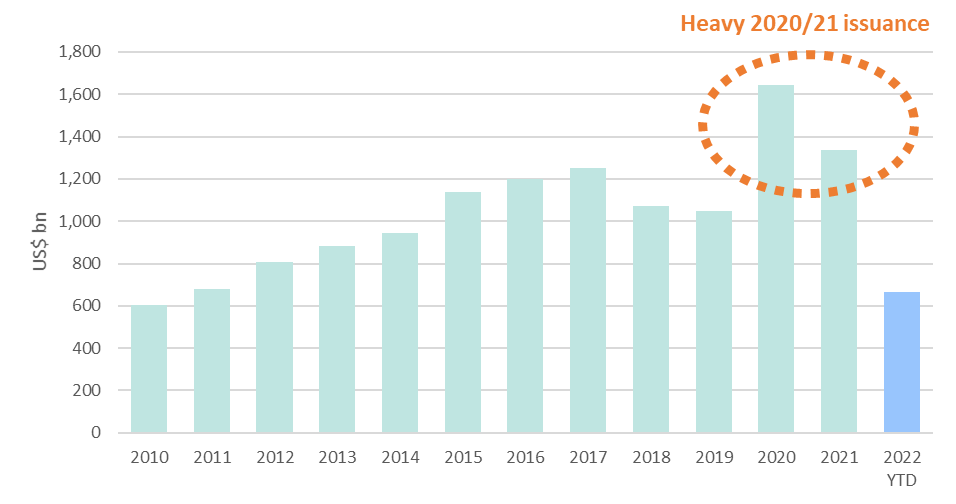

A high level of corporate debt issuance during the Covid crisis has bolstered the liquidity position of many firms. The chart below highlights the record levels of investment grade debt issued during 2020/21:

Source: Dealogic and Bloomberg, January 2020 to May 2022.

During this period, a large number of corporates in different countries and in various industry sectors locked in their financing needs at low rates. Interest coverage – a metric that measures how comfortably companies can service their debt repayment obligations – has risen following these capital raisings, suggesting default risk is not unduly concerning at this point.

Moreover, the recent trend in corporate bond issuance has been towards longer-dated securities. While the average lifespan of corporate bonds was previously around eight years, research now suggests this has risen to between nine and ten years1.

As a result, companies have greater flexibility and could come to the market for refinancing less frequently. Many are unlikely to require fresh debt capital for several years, in our view. In turn, higher official interest rates may not necessarily be an immediate concern for many companies.

And rating agencies have noticed…

This favourable backdrop has not gone unnoticed by the major rating agencies. In fact, rating agency upgrades have outpaced downgrades in 2022 to date2. This might provide investors with some additional reassurance that default risk remains relatively low. If so, the higher prospective returns from credit securities following recent spread widening could be increasingly appealing for long-term investors.

Will higher inflation make a difference?

The impact of current high inflation levels globally will not affect all firms equally. There is likely to be a divergence in operational performance across the corporate sector between companies operating in different regions and industries.

Those with strong market positions may be able to pass through higher costs to customers relatively easily, while others will find it more challenging to do so. As a result, the performance from credit securities in coming years will almost certainly vary.

Overall, the inflationary environment seems likely to make corporate earnings less predictable and will reward those investors able to differentiate between the winners and the losers.

1 Source: Bloomberg, as at 31 July 2022

2 Source: Moody’s, to 31 July 2022

Important Information

This document is not a financial promotion and has been prepared for general information purposes only and the views expressed are those of the writer and may change over time. Unless otherwise stated, the source of information contained in this document is First Sentier Investors and is believed to be reliable and accurate.

References to “we” or “us” are references to First Sentier Investors.

First Sentier Investors recommends that investors seek independent financial and professional advice prior to making investment decisions.

In the United Kingdom, this document is issued by First Sentier Investors (UK) Funds Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registration number 143359). Registered office: Finsbury Circus House, 15 Finsbury Circus, London, EC2M 7EB, number 2294743. In the EEA, issued by First Sentier Investors (Ireland) Limited which is authorised and regulated in Ireland by the Central Bank of Ireland (registered number C182306) in connection with the activity of receiving and transmitting orders. Registered office: 70 Sir John Rogerson’s Quay, Dublin 2, Ireland number 629188. Outside the UK and EEA, issued by First Sentier Investors International IM Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registration number 122512). Registered office 23 St. Andrew Square, Edinburgh, EH2 1BB number SC079063.

|  |

|---|