- Why load factors matter for airlines and for airports

- How motorways are investing to promote electric vehicles and reduce customer emissions

- Our expectations for further take-privates in transport infrastructure

- How airports are transforming land into destinations by building a square inside a circle

Benefits of the rapid recovery of airport and toll road volumes far outweigh the operational issues they now face as a result.

We expect higher load factors to compensate for airline capacity cuts, meaning traffic will continue to edge towards 2019 levels.

European toll roads have a positive role to play in the decarbonisation of the transport sector, providing both societal benefits and investment return upside.

I have recently returned from two weeks in Europe visiting over twenty global listed infrastructure companies, regulators and airlines. I witnessed first-hand the pent-up demand driving European airports towards 2019 traffic levels, a surge that has seen the market upgrading earnings forecasts for this year in response.

We believe the multi-year disruption to travel caused by the pandemic has led to a multi-year build-up in demand for travel. Whilst the economic environment may present challenges in the months ahead, we believe this pent-up demand bodes well for 2023.

Meanwhile, toll roads continue to see traffic above 2019 levels throughout Europe. This, combined with CPI-linked increases in tolls, is leading to modest earnings upgrades for these companies.

Airline cancel culture

Much has been made recently of the issues being experienced at airports around the world, with many struggling to handle the rapid rebound in passengers. There is no doubt that some airports are struggling, with summer flight capacity caps implemented at Amsterdam Schiphol, London Heathrow and London Gatwick airports.

Figure 1: Visiting Rome’s Fiumicino Airport Control Tower

Italian air traffic control operator ENAV is already seeing flight activity at 94% of 2019 levels

Source: First Sentier Investors

However, I observed that this certainly is not an issue being experienced at all airports. Some are far better positioned than others to handle the increased flow of passengers. Anecdotally, of the eight airports I visited and eight flights I took, I only experienced extended wait times at one airport, had one minor flight delay and had no flight cancellations.

Most impressive was Zurich Airport, where the longest wait time at security over the past couple of months was just twenty minutes, with an average wait time of between five and seven minutes. This is in stark contrast to the reports of multi-hour waits at a number of other airports in Europe.

Figure 2: Talking all things Zurich Airport

An airport tour with CEO, Stephan Widrig

Source: First Sentier Investors

So who do I blame?

The issues we are seeing are the result of headcount reductions in response to the pandemic, which in turn have affected both airline and airport operational capacity. Unfortunately scaling back up is not a simple task, largely the result of security clearance requirements as well as labour market constraints more broadly.

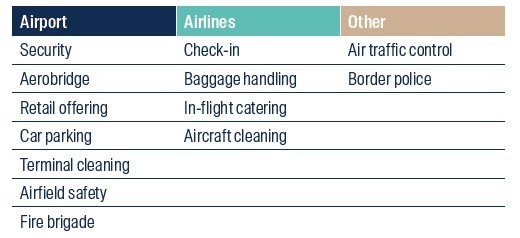

As you wonder who to curse the next time your baggage is lost or you spend 30 minutes waiting in line at security, it is worth highlighting at this point where the responsibilities lie for various roles in an airport. Not all airports are the same, but broadly the separation of responsibilities reflect something similar to the below.

Figure 3: The role of airports

Source: First Sentier Investors

As a result of this separation of responsibilities airport employees typically only account for 5-10% of all workers at the airport. The majority of headcount is linked to retail concessionaires, airlines and airline contractors, such as baggage handling companies. This highlights the fact that airport companies are very much delivering value from the infrastructure itself rather than via service-based activities.

Figure 4: Touring a busy Gatwick Airport with management.

LGW is owned by diversified French concessionaire, Vinci

Source: First Sentier Investors

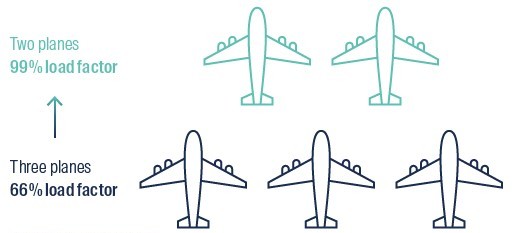

Beyond the operational issues, we believe that some flight cancellations are being driven by a concept known as ‘load factor optimisation’. A load factor refers to the percent of available seats being occupied by paying passengers.

Higher load factors via cancellations can allow airlines to improve their operating performance. This means airlines overcommit capacity to ensure they can achieve the highest possible number of passengers and then trim capacity to match the actual demand levels seen in bookings. This can continue right up until the day of your flight, with flights being bundled together where possible to maximise the profit per seat.

Figure 5: Load factor optimisation

Source: First Sentier Investors

So what does this mean for your next flight? We expect this trend to continue over summer, which means while your flight might get consolidated there remains very low risk of people not being able to get to their final destination. As we get closer to peak summer and the flights are increasingly full naturally due to demand, you can also expect this to ease.

Looking beyond the recovery

Ultimately we are confident that these issues are not going to be multi-year constraints on the ability of airports to grow volumes. So from a long-term investment perspective we focus our attention towards the constraints of the infrastructure itself, this being the capacity of the runways and terminals.

Figure 6: Inspecting Frankfurt Airport’s T3 Expansion

Source: First Sentier Investors

Prior to the pandemic a number of airports around the world had experienced the issues of both slot constraints (being the number of flights that can land at an airport on any given day) and terminal capacity limits (being the number of passengers that can be processed). With the strength of recovery this again becomes a focus point for airports, particularly for those leisure orientated airports that are already exceeding 2019 levels.

During my trip, Zurich Airport announced it is commencing planning for a major refurbishment and expansion project in response to the faster than anticipated demand. German peer Fraport has continued to press ahead with its new Terminal 3 project at Frankfurt Airport. This highlights the need for airports to look ahead 5-10 years, owing both to the regulatory implications of these projects, and to the complexities of building in a live airport environment.

Figure 7: Zurich Airport’s Dock A project

Source: Flughafen Zurich ©

This is particularly an issue at slot-constrained airports, where land or government constraints often prevent the airport from adding additional runways to allow more planes to land. JFK Airport in New York and London Heathrow Airport are both examples of airports that suffer from this slot constraint. The decline of the super-jumbo aircraft such as the Airbus A380 and Boeing 747 has further accelerated these issues, with the more fuel efficient Boeing 787s and Airbus A350s not capable of carrying the same number of passengers per take-off or landing slot.

As a result, we remain very conscious of the capex needs of airports in coming years as they change gears from COVID hibernation back to growth.

A green recovery

Whilst there is concern about the pressure that inflation places on consumers, it was clear in my discussions with companies and regulators that these concerns must be balanced with the need to continue on the path of decarbonisation. A European regulator described this in my meeting as the “path of least regret”. Regulators must work with these companies to find ways to continue investment whilst protecting affordability.

Infrastructure companies have a clear and important role to play in these discussions, as ultimately these companies require a social licence to operate in order to maintain and protect their monopoly or oligopoly market structure. French toll road and airport concessionaire, Vinci, highlighted this in my meeting by emphasising their openness to work with regulators to implement toll freezes as they did in 2015. This occurs in exchange for concession extensions or deferred toll increases, ultimately leaving the company no worse off but providing immediate relief to the consumer.

Figure 8: Eiffage & Atlas Arteria’s APRR Network in France

Source: APRR/La France vue du ciel

We believe these discussions provide a positive opportunity for toll road concessionaires such as Vinci, Eiffage and Atlas Arteria to negotiate investment plans for the decarbonisation of the French road network. The combination of a toll freeze agreement and ‘green’ investment plans would result in a material extension to the concession life that these companies have over their respective sections of the French road network.

But what do these green investment plans involve? These plans would significantly accelerate the availability of EV charging infrastructure on the network to alleviate range anxiety, as well as investment in projects such as free-flow tolling. This involves the removal of toll booths in exchange for electronic tolling, reducing carbon emissions from unnecessary braking and acceleration on the network.

Figure 9: EV charging station on Vinci’s French Autoroute Network, ASF

Source: Vinci

French motorway network APRR recently received approval for a €400 million investment plan. This plan included car parking facilities for ride-sharing, the creation of dedicated ride-share lanes and studies for further expansion of these measures to other parts of their network. Meanwhile, Vinci in late 2021 released a report that estimated €5-6 billion in investment would be required to decarbonise a 1,000km section of motorway. This implies an investment opportunity of up to €22-26 billion across their 4,400km Autoroute du Sud de la France (ASF) network in the South-West of France. We believe the immediate investment opportunity will be closer to ~€8-10 billion, which in turn could result in a ~8-10 year concession extension for the network.

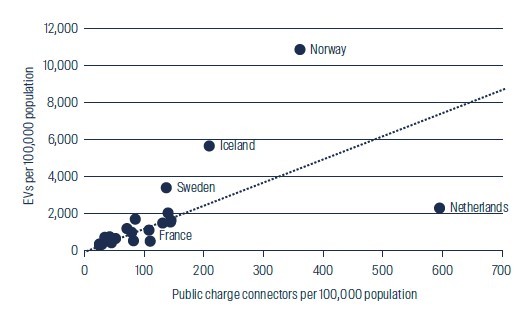

Figure 10: EV public charging infrastructure by country

Source: BNEF, First Sentier Investors as at 31 December 2021

Ultimately these investments are a win-win for the French government, the concession companies and the planet. This is particularly important for the French autoroute network, which despite being only 1% of all roads in France is responsible for 25% of road emissions due to the high traffic nature of these road networks1. These investments provide private capital to address the single largest contributor to transport emissions, with vehicle travel responsible for 95% of the sector’s emissions. Meanwhile the concessionaires benefit from the extended cash flow life from these assets via the concession extensions.

Privatisation Potential

A common question we have received from clients lately has been the concern that the asset class may be shrinking as a result of private equity and pension funds continuing to buy up listed infrastructure assets.

We would agree that this is a valid question to ask, following the recent acquisitions of Sydney Airport and Atlantia. Ultimately if private markets ascribe a materially higher value to a company’s assets than we do, we are willing sellers. We believe that Australian toll road company, Atlas Arteria and the French concessionaire to Eurotunnel, Getlink, are both examples of companies where similar takeovers could potentially play out in the short-to-medium term.

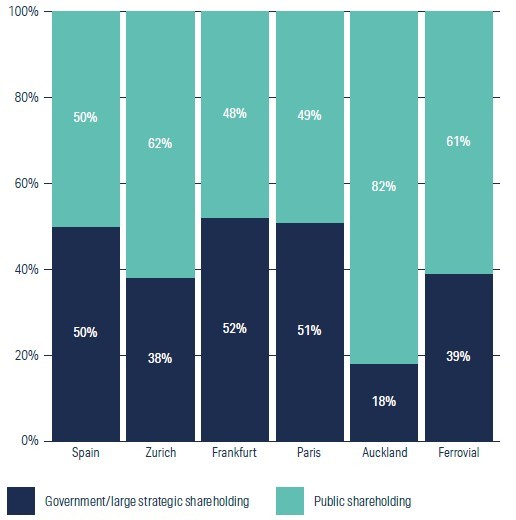

The natural question is then, could the universe disappear completely? As with any company, this is possible in theory. However, European airports have government ownership to varying extents and toll roads such as Ferrovial have large ‘blocking’ shareholders. These shareholders with significant control, along with foreign ownership restrictions, voting limits and other constraining structures make privatisation challenging for many of these companies. As a result, we expect the investable universe to maintain a healthy range of investment opportunities.

Figure 11: Airports & toll roads with government or large single strategic shareholdings

Source: Bloomberg as at 30 June 2022

The Circle @ Zurich Airport

Flughafen Zurich (Zurich Airport) owns and operates Switzerland’s largest airport via a 50-year concession ending in 2051. We believe there is significant unrecognised value in their assets, particularly their property assets.

I was fortunate to spend a day at Zurich Airport, meeting various members of its management team and touring both the airport assets and their recently completed commercial development, The Circle.

Figure 12: The Circle @ Zurich Airport

Source: Flughafen Zurich ©

The Circle is a 180,000 square metre mixed-use development incorporating office space, 540 hotel rooms, significant ground floor retail and six restaurants as well as the Zurich University Hospital. The project was completed in November 2020 and is a 51:49 joint-venture between Zurich Airport and Swiss Life, a life insurer with CHF 276 billion (USD $288 billion) in assets. The building is directly connected to the airport and landside retail precinct via a short underground walkway or via the above ground transport hub that serves 25,000 commuters each day.

Figure 13: Public Transport Hub Adjacent to the Precinct

Source: Flughafen Zurich ©

One of the key reasons we believe Zurich Airport’s real estate is so valuable is the close proximity to the city and positioning as a key hub for Northern Zurich. This is reflected in the fact that only ~50% of the 150,000 visitors to the airport each day are there for the purpose of flying, with the balance being commuters, shoppers and office workers. I travelled to the airport from the Central Business District (CBD) via both train and tram, with the journeys taking around 15 minutes and 35 minutes respectively. Zurich Airport is a logical base for not just industrial tenants but also for blue chip commercial tenants you might ordinarily find in a CBD. This thesis has played out in the leasing of commercial space; with marquee tenant signings including Microsoft, Oracle, SAP and Merck.

These global companies benefit from the connectivity that the airport provides not only to air travel but also to high-speed rail. The airport serves as a major hub for the Swiss rail network, with a station directly beneath the airport terminal. This connectivity allows travel to Basel in 90 minutes, Milan in 3.5 hours and Frankfurt in 4 hours.

Figure 14: Internal retail and dining precinct

Source: First Sentier Investors

We expect The Circle will provide a strong and stable earnings stream for Flughafen Zurich via long-term rental agreements that are tied to inflation. We see upside to current earnings as we believe this premium offering is likely to see leasing rates improve over time.

Most Interesting retail shop

The Square is a concept store from Volkswagen where electric vehicles from their various brands are displayed. The store is aimed at educating visitors on the process of going from a combustion engine to an EV; addressing concerns such as charging infrastructure in the home, range anxiety and the driving experience.

Figure 15: The Square at The Circle

Source: First Sentier Investors

1 Altermind ‘Decarbonising the Road; An Ecological Emergency’

Important Information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should consider, with the assistance of a financial advisor, your individual investment needs, objectives and financial situation.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material and we do not undertake to update it in future if circumstances change.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group. Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Limited, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors is a business name of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) is a business division of First Sentier Investors (Singapore).

- Japan by First Sentier Investors (Japan) Limited, authorised and regulated by the Financial Service Agency (Director of Kanto Local Finance Bureau (Registered Financial Institutions) No.2611)

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167)

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

|  |

|---|