Airports have seen phenomenal traffic growth as people prioritise travel and experiences in the face of cost‑of‑living pressures.

The rate of growth in the near‑term is seemingly not a demand story, but rather a question of whether airlines and aircraft manufacturers can keep pace with an insatiable demand to travel.

In the medium‑term we expect demand from baby boomers, millennials and Asia’s emerging middle class will continue to drive strong global traffic growth. We explore what this means for listed airport companies.

The state of flight

We have observed a three‑stage recovery of airline capacity since 2022. All of which have been acutely felt by travellers, both in terms of their patience and their hip pocket.

The first stage in 2022 and 2023 – by far the most challenging for travellers – was characterised by low levels of operational readiness for most airlines and airports. This led to low levels of flight availability, delays, cancellations and a poor overall travel experience. Airlines took advantage of the demand‑supply mismatch, with ticket prices hitting levels 20–40% higher than 2019.1

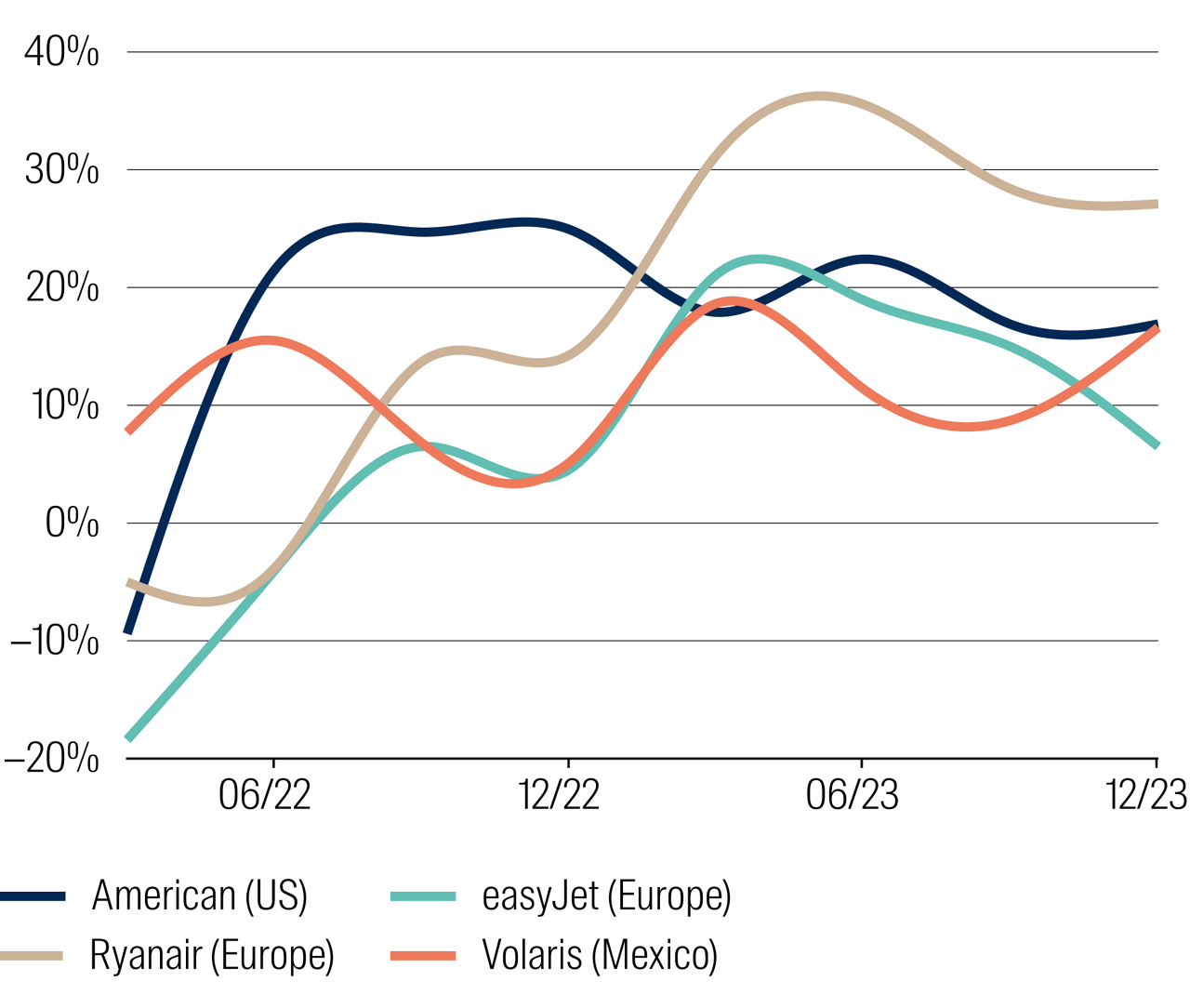

Then during late 2023 and 2024 we saw improvements in seat capacity as more planes returned to the skies and operational readiness improved. We saw low‑cost carrier (LCCs) such as Ryanair in Europe and Volaris in Mexico perform particularly well, with their operating agility and healthy balance sheets allowing them to move more quickly to capitalise on strong traveller demand. Unfortunately for travellers whilst the experience started to improve, ticket prices remained elevated. Strong traveller demand resulted in any additional capacity being quickly absorbed, allowing airlines to largely sustain the pricing gains they’d made.

Airfares vs 2019

Airfares based on revenue per available seat mile

Source: Company data.

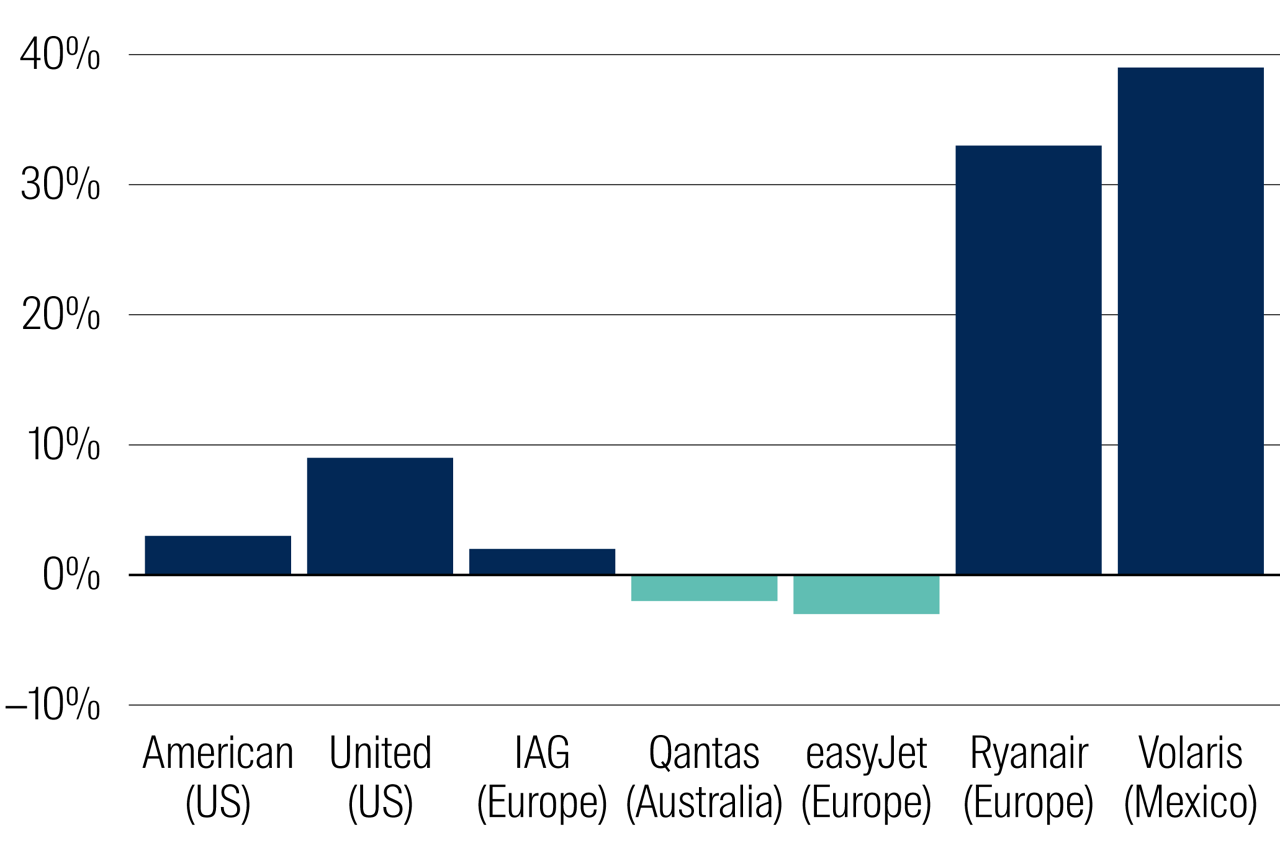

More recently, capacity and pricing growth have somewhat normalised. Pricing has even gone backwards in some regions. For example, the US has seen pricing declines of between 5% and 10% in periods through 2024 and 2025, driven in large part by overcapacity on leisure‑orientated routes. In Europe demand has continued to be robust and capacity additions have been modest, leading to strong pricing trends particularly during holiday travel periods.

2024 capacity vs 2019

Capacity = Available seat miles/available seat kilometres

Source: Company reports.

Stuck in a holding pattern

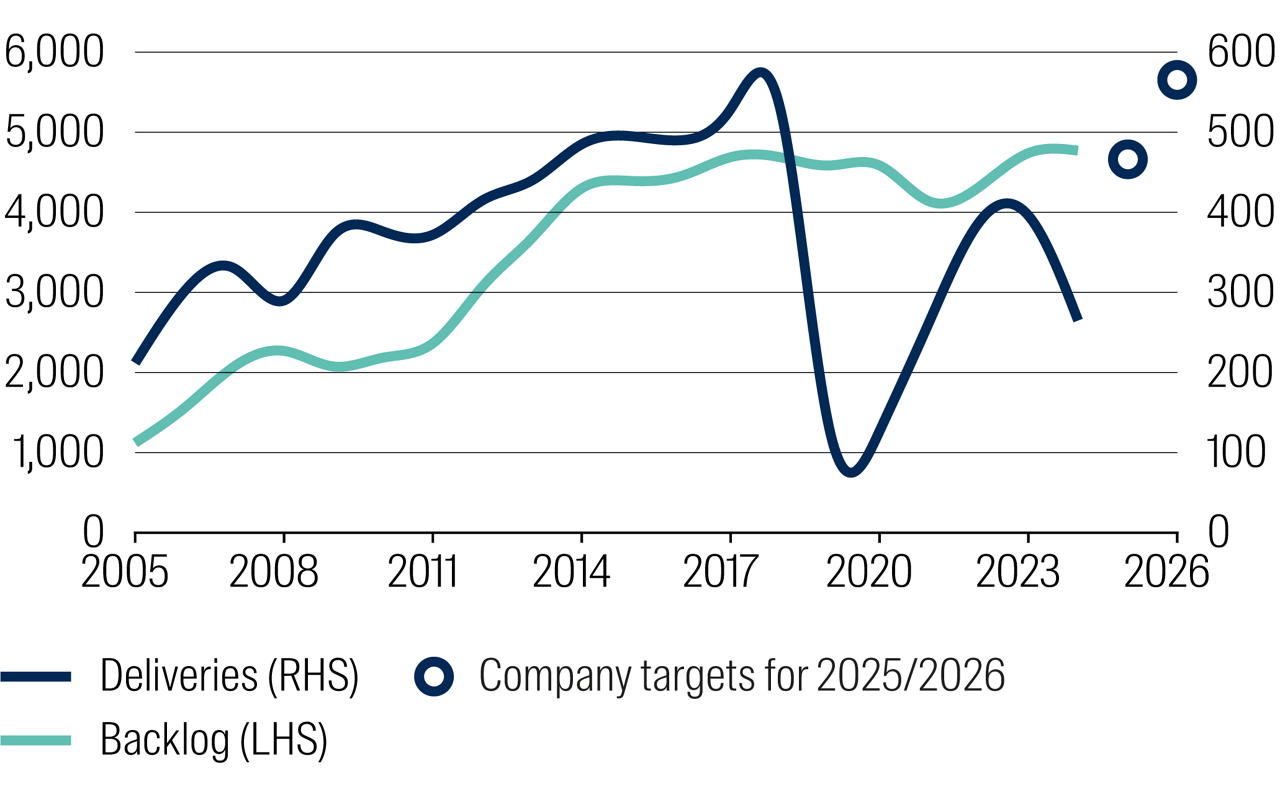

The key constraint we see to further upside to traffic growth in the near‑term is the lack of new aircraft becoming available to continue to satisfy demand growth. The world’s two dominant aircraft manufacturers, Boeing and Airbus, remain nowhere near their previous rates of aircraft production. Total industry output is still running 30% below the highs seen in 2018. This hasn’t stopped them from taking orders for new planes though, with outstanding orders for new planes reaching a record high of over 17,000.2

Boeing’s 737‑Max, the aircraft responsible for much of the world’s short‑haul traffic growth, has over 4,500 outstanding orders alone. Even if Boeing were to lift their production rates from the currently capped 38 aircraft deliveries per month to the targeted 47 deliveries per month, their order book would still take more than seven years to clear.

Aircraft demand outpacing supply capacity

Boeing 737 order backlog and deliveries

Source: Boeing.

Data as at 30 September 2025.

We expect these capacity growth headwinds to ease in 2027 as aircraft production rates improve, allowing airlines to receive new aircraft and put them to work. This should see downward pressure on ticket pricing, with the additional capacity leading to a more competitive market for airlines. Both of which bode well for traffic growth.

As a result, we are positioning the portfolio towards those airports where earnings growth is not predicated on significant capacity additions in 2026. We find this in Zurich Airport and in Groupe ADP’s Charles De Gaulle and Orly airports in Paris. We believe the market has suitably conservative expectations on traffic growth for both companies, and we see earnings upside potential from other areas of their businesses such as retail and their international operations.

Airbus forecast of demand growth

Fleet in service (# aircraft)

Source: Airbus GMF 2025, Cirium May 2025.

SKI season

As we see these supply‑side constraints ease our expectation is that strong demand growth will continue. The trends of baby boomers ‘spending the kid’s inheritance’ (SKI) and millennial/ Gen‑Z ‘fear‑of‑missing‑out’ (FOMO) travel should continue to fuel growth.

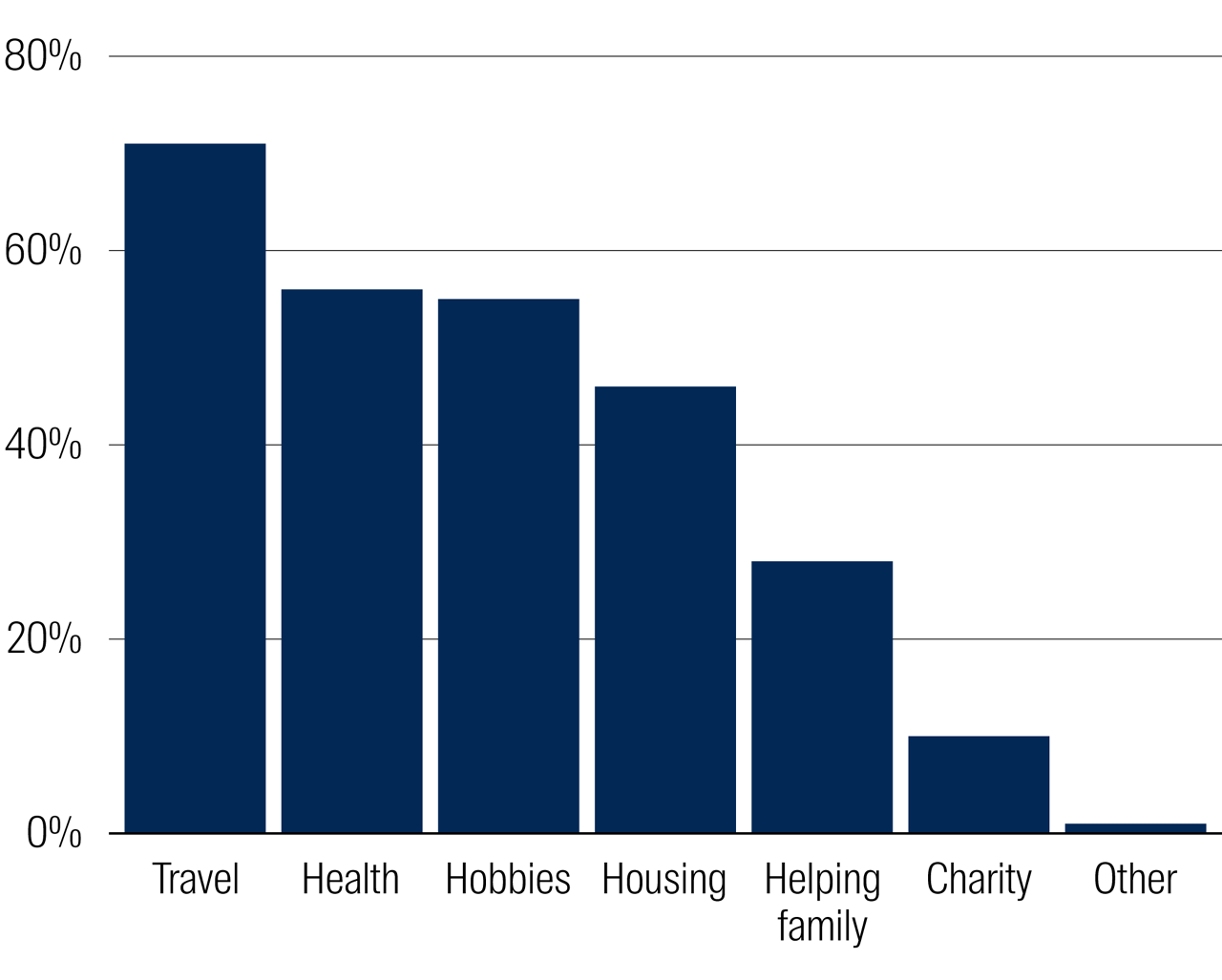

The SKI phenomenon has been cited by airlines as a positive source of growth, particularly when it comes to the strong performance they have seen in their premium (premium economy/ business/first class) cabins. A recent survey of US retirees found that 63% of Americans nearing retirement saw travel as an important retirement goal. Another survey found that just 6% of retirees felt leaving a financial inheritance was more important than creating travel memories. The same survey found 68% of retirees don’t worry about spending their children’s inheritance when travelling.3

What are your spending priorities for retirement?

Survey of 2,000 Australians

Source: Equipsuper.

Data as at July 2024.

At the opposite end of the age spectrum, we find that younger generations are prioritising travel more than ever before. A recent McKinsey report noted that 76% of Gen Zers agreed with the statement ‘I am more interested in travel than I used to be’. Even more surprisingly, just 15% said they were trying to save money by reducing the number of trips they go on.

The combined impacts of home ownership affordability challenges, climate anxiety and social media ‘travel influencers’ are all driving this shift. Leading the FOMO generation to live for today rather than save for tomorrow.

We see these two generational shifts as structural rather than cyclical drivers of traffic demand growth, helping to drive long‑run traffic growth expectations higher. This is in turn creating a multi‑year earnings and valuation uplift opportunity for the airport sector.

Indi‑go global

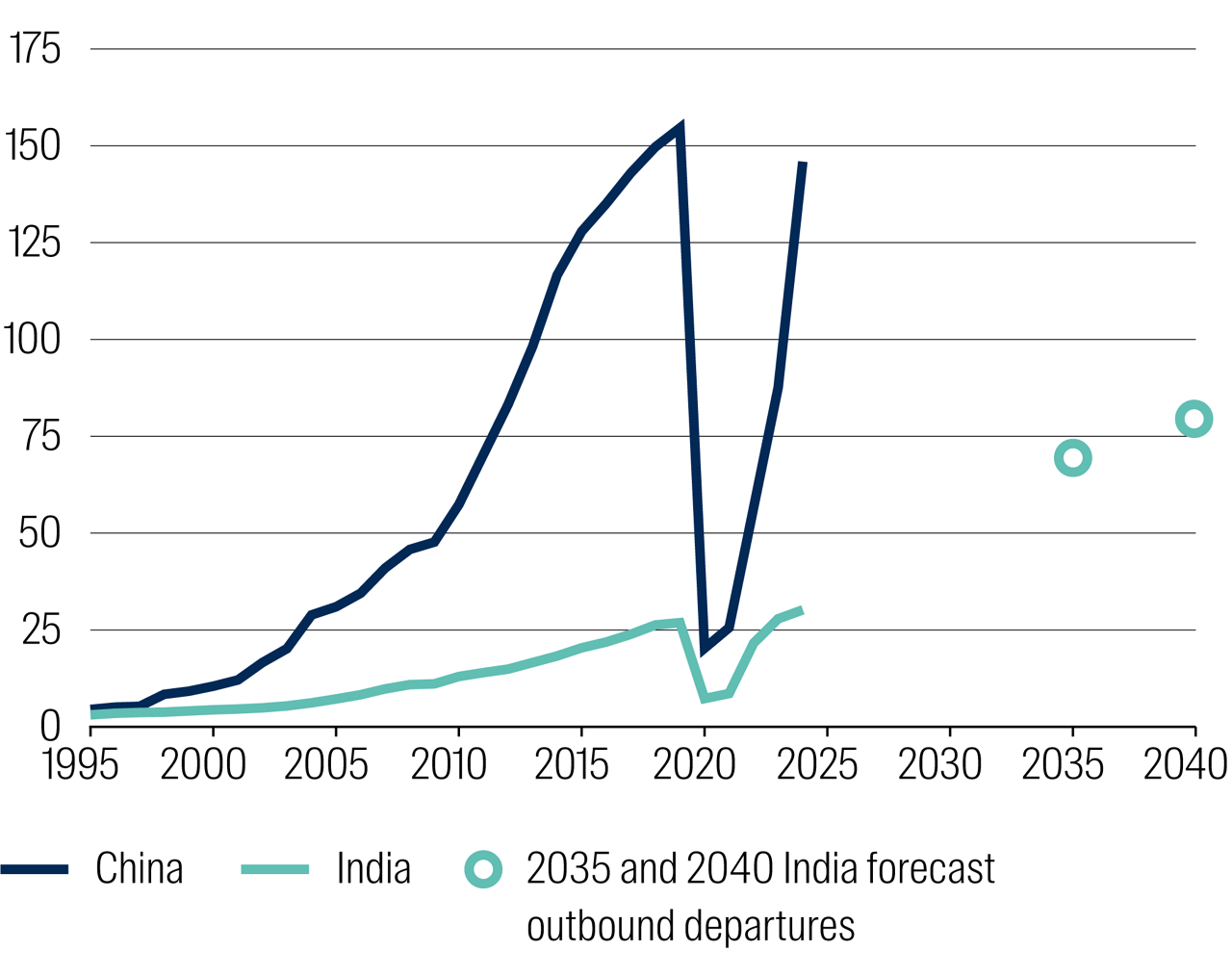

In the 1990s global tourism growth was fuelled by demand from Japanese tourists to see the world. Then we saw the rise of China’s middle class in the mid‑2000s up until the pandemic.

Looking forward we believe the story will undoubtedly be outbound tourism growth from Indian travellers. At the same time, we believe that growth from China is far from over. We anticipate that China’s emerging middle class will once again support strong travel demand growth as the country’s domestic economic outlook improves. As a result, we expect dual tailwinds out of Asia as these two countries with a combined 2.8 billion people drive global tourism growth.

Back to the future

Outbound departures (millions)

Source: World Bank, CEIC, Travel China Guide, McKinsey, DFAT.

Data as at 30 September 2025.

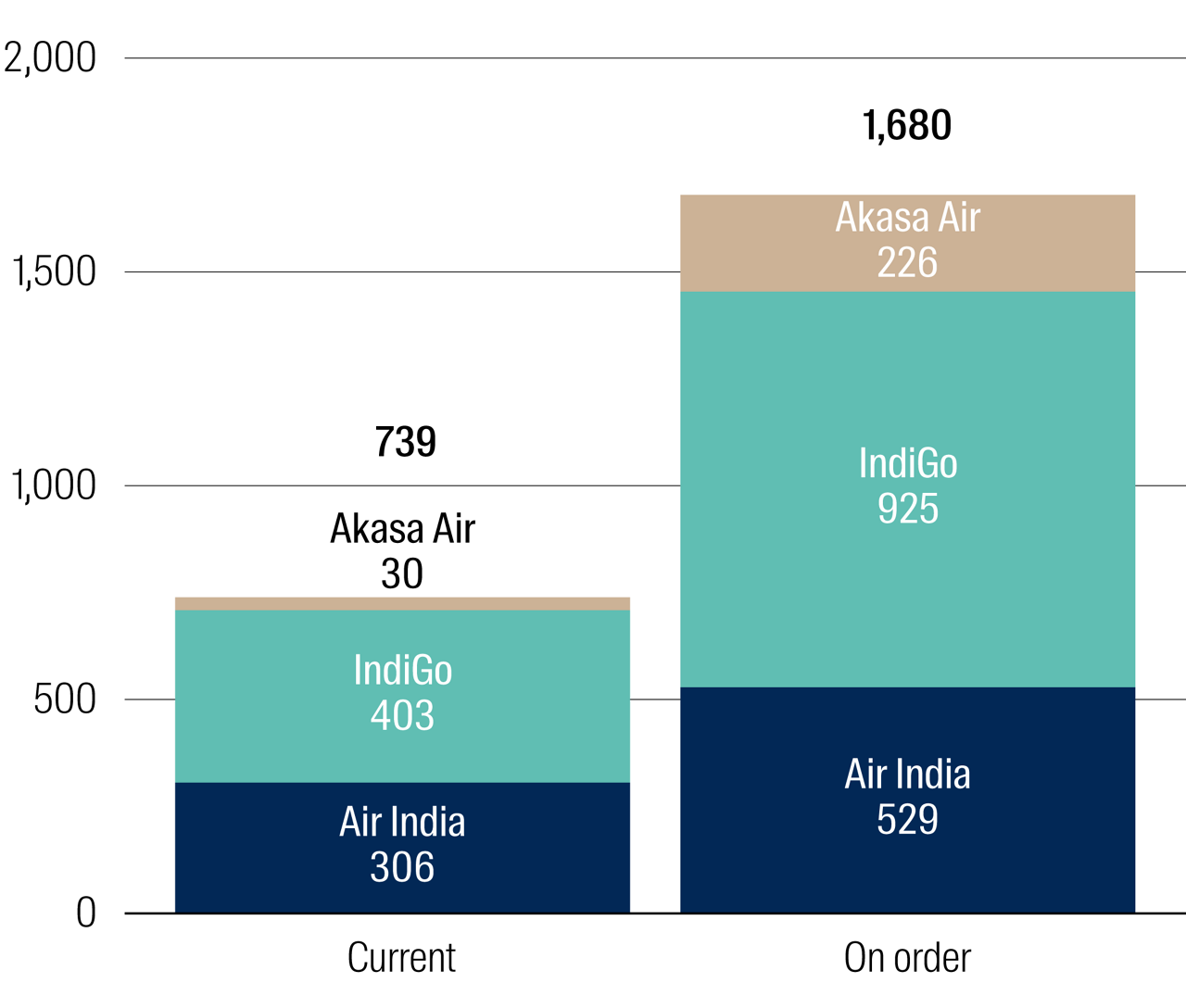

Indian airlines are ready to meet this demand as well. As highlighted below, the big three local airlines have a combined 1,680 new planes on order.4 This compares to a combined current fleet of 739 aircraft. A phenomenal increase in capacity even once you assume retirements of some of the existing fleet. As a result, once the aircraft manufacturer issues previously noted are resolved, this is the region where we expect to see the most significant further acceleration in traffic growth.

Growth in aircraft fleet in India

Source: FlightRadar24, Company reports.

Data as at 30 September 2025.

This is one of the reasons we see significant valuation upside in portfolio companies Flughafen Zurich and Groupe ADP.

Flughafen Zurich, whose primary activity is the operation of Zurich Airport, recently completed the development of Delhi’s Noida International Airport. This airport is expected to have 8 million passengers in its first full year of operations, which we believe is an unprecedented level of growth for a new secondary airport. We expect Flughafen Zurich will be able to realise significant value from their investment in the near‑term via a minority stake sale to an institutional investor looking for exposure to this significant growth in Indian tourism.

Noida International Airport

Source: First Sentier Investors

Groupe ADP is another portfolio company that identified India as a growth market early, acquiring a 49% interest in leading listed Indian airport operator GMR for €1.36 billion in February 2020. This stake today is worth over €4 billion based on market pricing,5 a 3x increase on their initial investment. We believe the market is placing very little value on this investment currently; something which we believe could shift as GMR management increasingly focuses on returning capital to shareholders via dividends as the company moves out of its capital‑intensive investment phase.

Building for growth

We are seeing airport companies positioning for this growth, with increased investment in the infrastructure to accommodate the additional passengers they expect to serve. Within our universe, Auckland Airport, ADP’s Paris airports, Aena’s Spanish airports, Vinci’s Gatwick Airport, Vinci’s Lisbon Airport, Zurich Airport, and all of Mexico’s three main airport operators are entering large investment programs.

Portfolio company GAP is the operator of twelve airports in Mexico, including the high growth airports of Guadalajara, Tijuana and Los Cabos. In late 2024 they agreed with the regulator to a US$2.4 billion capex program. This will enable them to expand their airports to cater to the significant demand growth they are seeing. In exchange for this investment, the local aviation regulator approved a ~30% increase in the aeronautical fees they are allowed to charge to the airlines. This highlights the strong earnings growth we are seeing as airports look to expand capacity in order to serve this passenger demand growth.

Zurich Airport’s Dock A refurbishment & expansion project

Source: Zurich Airport

Zurich Airport is in the early stage of planning the reconstruction and expansion of their Dock A terminal infrastructure and control tower, which is approaching the end of its useful life. The new CHF1 billion+ terminal infrastructure will allow Zurich Airport to more efficiently handle the processing of passengers. This should both lift the terminal’s passenger capacity and improve the overall customer experience and the retail offering being provided to travellers.

This highlights how the expansion benefits for airport companies are two‑fold, providing upside to aeronautical charges as well as improving the quality of the retail offering. These commercial segment earnings largely fall outside the regulated operations of the airport, allowing airport operators to generate returns over and above their regulated return.

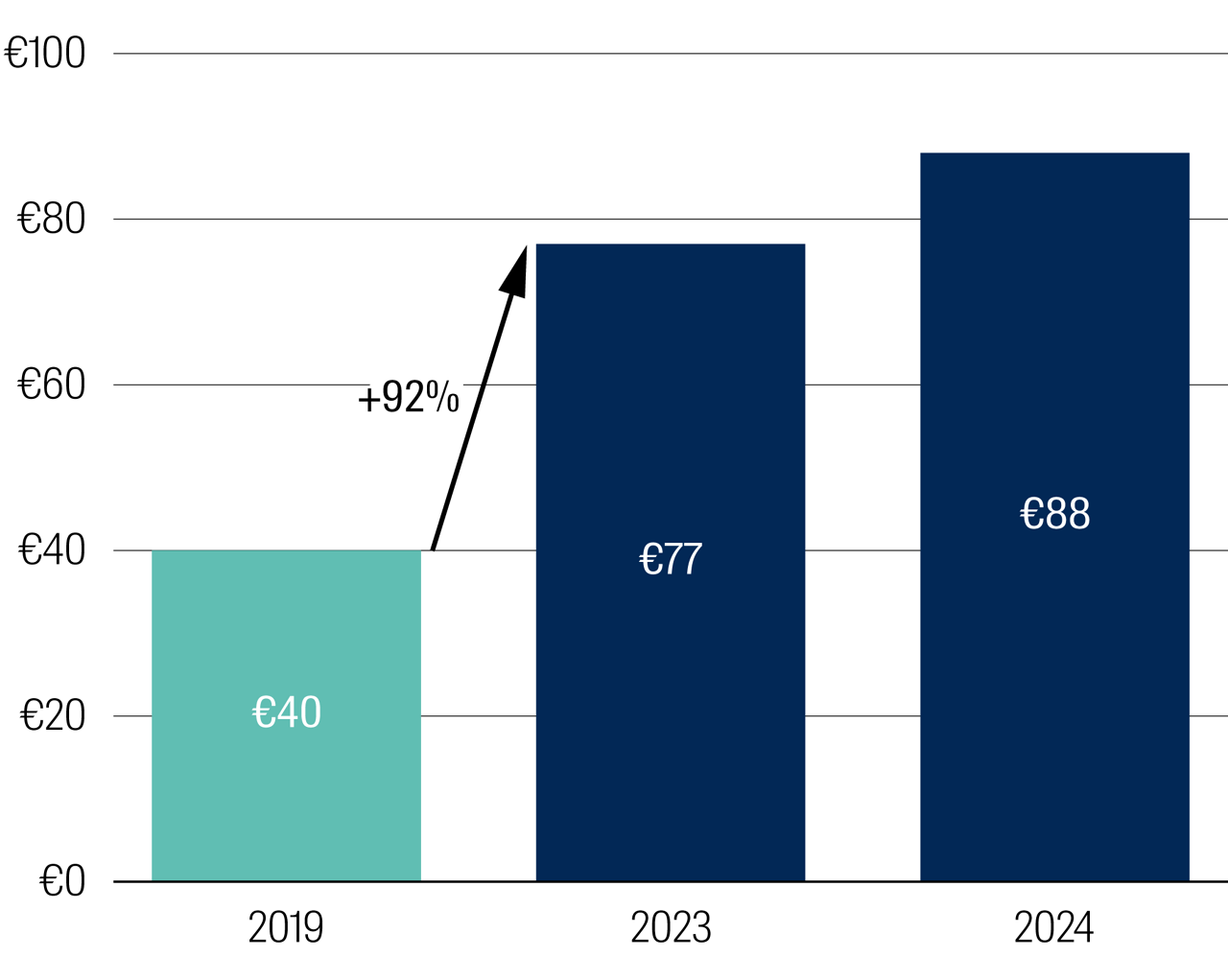

New or renovated terminals can lead to a meaningful step‑change in commercial revenues, as a higher quality retail offering drives higher sales per passenger (SPP). Most recently we saw this with the Terminal 1 renovation at Groupe ADP’s Charles De Gaulle Airport. By the end of 2023, ADP had seen a 92% increase in the SPP for Terminal 1 following the opening of the refurbished terminal in 2022.

Paris CDG Terminal 1

Sales per passenger (€)

Source: Company reports; First Sentier Investors estimates.

Data as at 30 September 2025.

This becomes an even more impressive figure when you factor in much lower contributions from high‑spending Chinese passengers in 2023/2024, who in 2019 accounted for only 2.1% of the traffic but 15.4% of retail revenues.

Conclusion

In summary, we are seeing significant traffic momentum from generational trends such as SKI and FOMO that we believe are here to stay. This, coupled with growth in travel demand out of Asia, has led to a meaningful step‑change in the long‑run passenger traffic growth outlook for a number of airports.

While near‑term traffic growth may be constrained by aircraft availability, the long‑term nature of infrastructure means these companies are planning for the long‑term growth now. We believe this will be a positive multi‑year earnings growth driver for the airports sector.

1 Company Reports

2 IATA

3 Grey Gap Year Report 2025, Australian Seniors

4 Boeing and Airbus company reports

5 Bloomberg; as at 3rd October 2025.

Global Listed Infrastructure

Infrastructure powers the world we live in – and when it comes to on-the-ground research, our team can be found on site

Investing in global listed infrastructure can offer inflation-protected income and steady capital growth from real assets delivering essential services. We search for best-in-class assets worldwide with high barriers to entry, structural growth and pricing power.

Read our latest insights

Important Information

This material is a financial promotion/marketing communication but is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure.

Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward‑looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Group.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward‑looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Group portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Group.

Selling restrictions

Not all First Sentier Group products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Group in order to comply with local laws or regulatory requirements in such country.

About First Sentier Group

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Group, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names AlbaCore Capital Group, First Sentier Investors, FSSA Investment Managers, Stewart Investors and RQI Investors all of which are part of the First Sentier Group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Group.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Australia and New Zealand by First Sentier Investors (Australia) IM Ltd, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

- European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in

- Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Group, First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this advertisement or material has not been reviewed by the Monetary Authority of Singapore. First Sentier Group (registration number 53507290B), First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), RQI Investors (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business names of First Sentier Investors (Singapore).

- United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

- United States by First Sentier Investors (US) LLC, registered with the Securities Exchange Commission (SEC# 801‑93167).

- other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (FCA ref no. 122512; Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB; Company no. SC079063)

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Group