This is a financial promotion for The First Sentier Global Property Securities Strategy. This information is for professional clients only in the UK and EEA and elsewhere where lawful. Investing involves certain risks including:

- The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

- Currency risk: the Strategy invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Strategy and could create losses. Currency control decisions made by governments could affect the value of the Strategy ‘s investments and could cause the Fund to global bond defer or suspend redemptions of its shares.

- Single sector risk: investing in a single economic sector may be riskier than investing in a number of different sectors. Investing in a larger number of sectors helps to spread risk.

- Single country / specific region risk: investing in a single country or specific region may be riskier than investing in a number of different countries or regions. Investing in a larger number of countries or regions helps spread risk.

- Property securities risk: the Strategy invests in the shares of companies that are involved in property (such as real estate investment trusts) rather than in property itself. The value of these investments may fluctuate more than the underlying property assets.

- Emerging market risk: Emerging markets tend to be more sensitive to economic and political conditions than developed markets. Other factors include greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities.

For details of the firms issuing this information and any Strategies referred to, please see Terms and Conditions and Important Information.

For a full description of the terms of investment and the risks please see the Prospectus and Key Investor Information Document for each Fund.

If you are in any doubt as to the suitability of our funds for your investment needs, please seek investment advice.

Introduction

The outlook for the global economy and financial markets looks more uncertain today than it has for a long time. Both interest rates and inflation have risen sharply. There is a growing consensus that much of the world will shortly be experiencing slowing economic growth. Understandably, investors are asking what their options are. With a wide array of asset classes available, which are best placed to offer investors resilience in the current environment, but also sustainable investment opportunities?

For investors seeking reliable income flows in addition to capital appreciation, property has historically, and likely will continue to be, a prime focus. In this paper the principal attractions and avenues for investment into the asset class will be examined and the case made that now is an attractive point for investors to consider listed property.

Further, the ‘why now’ case for listed real estate is bolstered by recent sharp sell-offs in the sector creating clear dislocations with core private funds. This relationship will be examined in this paper as we highlight the investment opportunity in listed property as both a compliment and a preference to property as an investment.

'Recent sell-offs in the sector have created clear dislocations'

Choosing how to invest

Before considering the investment merits, it is worthwhile considering the two main routes into property-investment: listed property (REIT’s) or private real estate (unlisted property funds). There are pros and cons for both with the main differences relating to liquidity and flexibility. The key characteristics of both are:

Direct/private property

- Lower correlation with equities and REITs in the short term and higher correlation to REITs in the long term

- Valuations based on Net Asset Value rather than the stock market

- Liquidity varies:

- Open ended private property funds: investors are offered a liquidity facility where they can redeem part or all of their units in the fund at regular or certain times during the life of the fund. Funds are still subject to ‘gating’ clauses

- Closed end private property funds: inflexible and illiquid as physical assets need to be sold to realise investments or until the fund ends

- Typically invested in traditional property types (office, residential and retail), more exposed to disruption than the alternatives property sector available in the listed universe

- High transaction costs

Listed property

- Liquid alternative to direct property investment, REITs are listed on equity markets

- Flexibility to move into different real estate sectors and regions

- De minimis transaction costs

- Greater transparency with tighter corporate governance regulation. Better corporate governance is generally correlated to increased investment outcomes

- Assets within the REIT universe provide access to alternative property sectors such as data centres, healthcare, residential and self-storage facilities

- Less volatile than equities1, but more volatile than direct property funds (see chart 1)

Chart 1: 18-Month Beta* Listed Property vs Direct Property

Disclaimer: FTSE EPRA NAREIT Developed Index vs INREV Global Real Estate Fund Index. All data in USD terms and as at 31 March 2023. Past performance is not indicative of future performance. Source: Factset and inrev.org

* Beta is a measure of the volatility of a security or portfolio compared to a market as a whole.

Chart 2: 18 month Rolling Beta of FTSE EPRA NAREIT Developed Index vs MSCI world index (as at 31 March 2023)

18 month rolling Beta of 0.89 for FTSE EPRA NAREIT Developed index vs MSCI world index. All performance data is in USD. Data from FTSE EPRA NAREIT Developed index inception date 31/01/1990 to 31 March 2023. Source: First Sentier Investors.

- Natural inflation hedge (stable cash flows, pricing power)

Chart 3: Listed Property vs Direct Property Funds by asset type

Listed Property

- Convenience Retail Shopping Centres

- Medical Office Buildings

- Life Science Assets

- Apartments for Rent

- Detached Housing for Rent

- Land Lease Communities

- Student Accommodation

- Hotels and Leisure Assets

- Logistical Centres

- Data Centres

- Self-Storage Facilities

- Seniors Housing Assets

- Private Hospitals

- Shopping Malls

- Suburban Office Buildings

- CBD Office Buildings

Direct Property

- Office Buildings

- Retail Shopping Centres

- Industrial Warehousing

‘The argument for listed property Is currently compelling’

With liquidity being a key attraction in markets with heightened volatility, the flexibility to move between property segments which may have different supply and demand dynamics and appealing valuations relative to history make the argument for listed property more compelling.

Understanding liquidity

As noted above, liquidity is an important consideration for investors. Within certain markets this has been a core issue during periods of volatility where private real estate funds have ‘gated’ their fund preventing investor redemptions.

This is typically the case in open-ended funds, where the funds liquidity facility is exhausted by mass redemption requests. Recently this occurred in periods such as the Global Financial Crisis, the 2016 UK Brexit vote, during the Covid period and may now occur again as rising interest rates puts pressure on direct property valuations.2

The realisation that a direct property fund cannot instantly sell a quarter of a shopping mall to meet redemption requests became a stark reality. This is due to the complex nature of property transactions being inherently less liquid than funds that invest in more readily traded assets such as listed equities, listed property and bonds.

Listed Property – the attractions

With listed property offering investor’s liquid property exposure to high quality assets across many property subsectors, what other attractions does this asset class offer? There are several core characteristics of listed property that reinforce the ability to deliver resilient cash flows together with long-term capital appreciation:

- Dependable cash flow

REITS tend to generate stable cash flows due to the revenues being derived from contracted rental income streams from a large array of property types.

The stable cash flows allows the REITs to be able to continually provide attractive dividends to their shareholders through the cycle. This is demonstrated in Chart 4 below where Global Listed Properties dividend yields are shown to be generally higher than Global Bonds and Global Equities over time.

Chart 4: Dividend Yield (%) Over time

Disclaimer: Data as at 31 March 2023. Global Reits as represented by the FTSE EPRA Nareit Developed index. Global Equities as represented by the MSCI World index. Global Bonds as represented by Bloomberg Global Aggregate Bond Index. All data is in USD. Source: First Sentier Investors, for illustrative purposes only.

- Leveraging growth

Listed property securities funds invest in higher quality assets and across multiple property types and regions that direct property funds may not have access to.

The asset diversity and quality pays dividends in generating capital growth within a listed property portfolio. The tenant base of a REIT often carries less risk than the overall property market, given the higher quality assets. Direct property funds often have relatively concentrated sector exposures and lack diversity and have greater tenant concentrations.

The asset types within the listed property universe such as biotech laboratories, data centres, student accommodation, self-storage facilities and logistics warehouses offer exposure to structural growth themes. These assets tend to have lower economic sensitivity with operating fundamentals driven by societal change, adoption of technology, growth in data consumption and the growth in pharmaceutical research and development etc. This is an important distinction between listed property and direct property funds, with listed property dividends consistently growing at a faster pace.

‘Listed property offers exposure to High growth themes’

An inflation hedge?

Many property types offer an inflation hedge to investors.

- Some property types have built in clauses in their rental contracts automatically increasing rents on an annual basis. These contracts can either be fixed in nature (usually c.2-3%) and/or tied to a published inflation rate or a mixture of both which may take pricing floors or caps into consideration. Over the shorter time periods these lease clauses assist in passing higher costs through to the tenants. However, for the inflationary hedge to be sustainable, the property requires pricing power. Without pricing power the inflationary hedge will not be sustainable and could lead to tenant default and/or material falls in rents at the end of the lease.

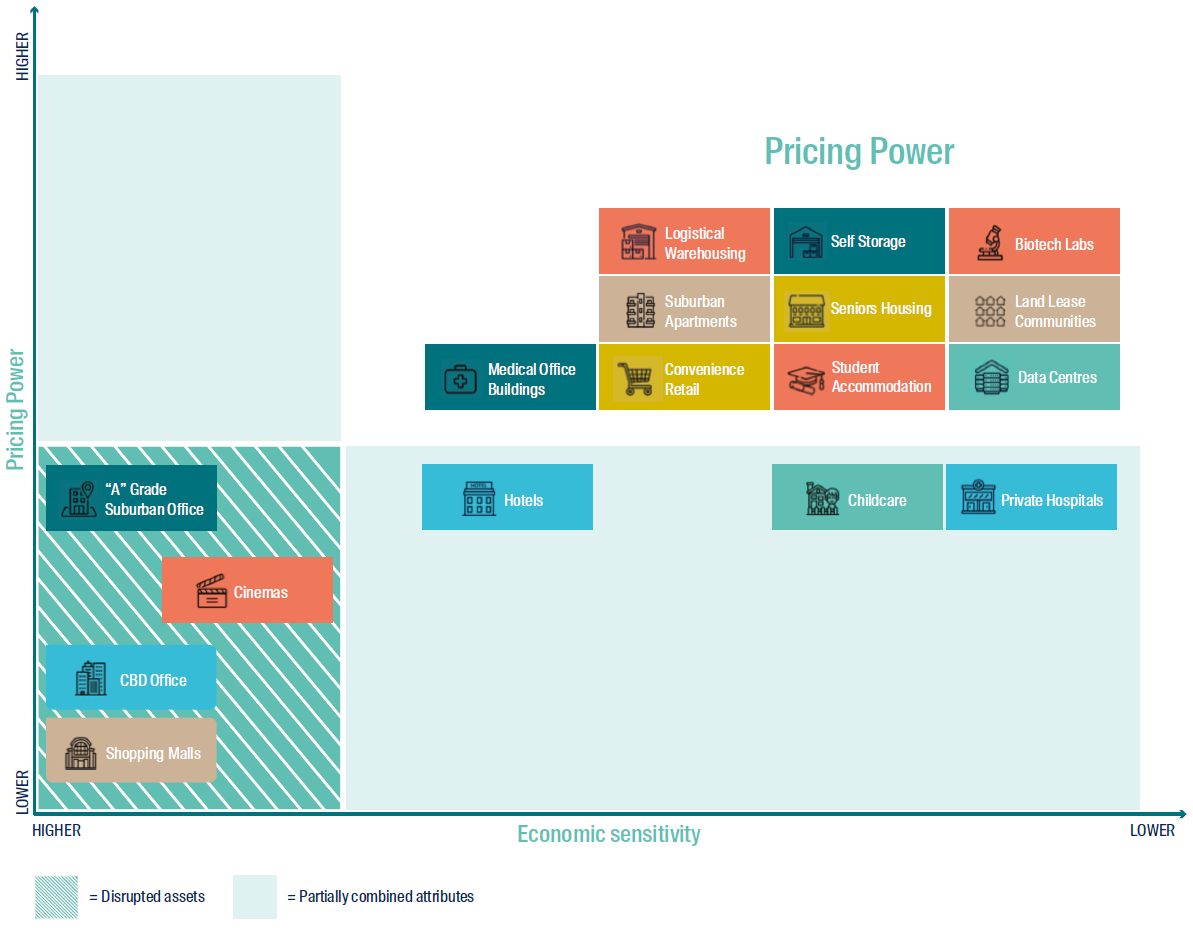

- Assets that are able to maintain ‘pricing power’ (see Chart 5 below) will be able to pass through inflationary pressures to tenants, providing a natural sustainable inflationary hedge driving revenue growth. Rising inflation also increases the replacement cost of property assets and increases barriers-to-entry, reducing supply. Limiting supply further underpins market rental growth and supports property valuations.

Chart 5: Pricing power within the Listed Property universe by asset type

Source: First Sentier Investors, for illustrative purposes only.

As shown in the chart above, the majority (+90%) of the listed property sectors assets sit in the top right quadrant, offering strong pricing power driving the inflationary hedge with low economic sensitivity.

Performance with rising interest rates?

Rising interest rates impact property valuations due to present-value calculations. However, rising interest rates tend to be accompanied by rising inflation. Those assets with pricing power to capture the inflationary hedge will be far better placed to mitigate the valuation effect of higher interest rates. The direct property funds tend to be exposed to old world traditional assets such as office buildings and shopping malls. These assets are disrupted, they do not offer an inflationary hedge and have high economic sensitivity. It’s these assets that tend to experience the greatest valuation falls as interest rates increase and this has certainly been the case in the current cycle.

- With the recent increase in interest rates, the First Sentier Global Property Securities strategy was sold off to a greater extent than private real estate during 2022 as demonstrated in Chart 8 below. This is not intuitive given the strategies exposures to assets that are not as exposed to valuation falls. Albeit history tells us that the strategy typically leads private real estate in both sell-off and recovery during recessionary periods. This is due to a lag effect in the valuations of unlisted assets. This lead-lag effect can create significant pricing dislocations in the short and medium terms (see Charts 6 and 7). Past performance through these periods’ highlights that the strategy subsequently delivers higher investor returns as direct property valuations continue to moderate.

Chart 6: First Sentier Global Property Securities Composite v Direct Property performance

Covid Period (December 2019 to December 2021)

First Sentier Global Property Securities Composite (net) versus INREV Global Real Estate Fund Index. All data in USD terms. Data from 31 December 2019 to 31 December 2021. Source: First Sentier Investors.

Chart 7: First Sentier Global Property Securities Composite v Direct Property

Performance comparison – Global Financial Crisis Period (December 2007 – December 2013)

First Sentier Global Property Securities Composite (net) versus INREV Global Real Estate Fund Index. All data in USD terms. Data from 31 December 2007 to 31 December 2013. Source: First Sentier Investors.

Changes to monetary policy in early 2022 led to a material sell down of the listed property sector, which created a discrepancy in performance between the strategy and the direct property sector as seen in Chart 8 below.

Chart 8: First Sentier Global Property Securities Composite v Direct Property

Performance comparison since inception

Disclaimer: Results do not reflect the deduction of management fees and other expenses. A client’s return will be reduced by the effect of management fees and expenses. First Sentier Global Property Securities Composite (gross) versus INREV Global Real Estate Fund Index. All data in USD terms. Inception date is 1 October 2006. Past performance is not indicative of future performance. Source: First Sentier Investors and Factset as at March 31 2023.

Conclusion

With financial markets adjusting to both higher interest rates and elevated inflation, it is not surprising many asset classes have experienced falling valuations. This has led to Listed property trading at a large valuation discount to direct property and also to its net asset value. With the strategy’s high asset quality, dependable inflation hedge and superior liquidity in conjunction with the current valuation dispersion, offers investors a compelling alternative to direct property funds.

Footnotes

1 See chart 2. 18 month rolling Beta of 0.89 for FTSE EPRA NAREIT Developed index vs MSCI world index. All performance data is in USD. Source: First Sentier Investors.

2 Reference: Fitch Ratings

Important Information

This document has been prepared for informational purposes only and is only intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document and does not constitute an offer, invitation or investment recommendation to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any material contained in this document.

This document is confidential and must not be copied, reproduced, circulated or transmitted, in whole or in part, and in any form or by any means without our prior written consent. The information contained within this document has been obtained from sources that we believe to be reliable and accurate at the time of issue but no representation or warranty, express or implied, is made as to the fairness, accuracy, or completeness of the information. We do not accept any liability whatsoever for any loss arising directly or indirectly from any use of this document.

References to “we” or “us” are references to First Sentier Investors a member of MUFG, a global financial group. First Sentier Investors includes a number of entities in different jurisdictions. MUFG and its subsidiaries do not guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk including loss of income and capital invested.

If this document relates to an investment strategy which is available for investment via a UK UCITS but not an EU UCITS fund then that strategy will only be available to EU/EEA investors via a segregated mandate account.

In the United Kingdom, issued by First Sentier Investors (UK) Funds Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registration number 143359). Registered office Finsbury Circus House, 15 Finsbury Circus, London, EC2M 7EB number 2294743. In the EEA, issued by First Sentier Investors (Ireland) Limited which is authorised and regulated in Ireland by the Central Bank of Ireland (registered number C182306) in connection with the activity of receiving and transmitting orders. Registered office: 70 Sir John Rogerson’s Quay, Dublin 2, Ireland number 629188. Outside the UK and the EEA, issued by First Sentier Investors International IM Limited which is authorised and regulated in the UK by the Financial Conduct Authority (registered number 122512). Registered office: 23 St. Andrew Square, Edinburgh, EH2 1BB number SCO79063.

Copyright © (2023) First Sentier Investors

All rights reserved.